Morning FX

1. Fundamentals: The pattern of a strong U.S. and weak Europe continues to deepen

This week is a major one for the release of U.S. employment data, and the White House seems eager to showcase its achievements: On Monday evening, Hassett stated, “Indicators suggest the jobs report will be strong again,” and on Tuesday evening, Boushey said “If June’s employment data is very strong, it would not be surprising,” directly signaling to the market that U.S. employment is robust. Due to this advance hint, the market showed almost no reaction to Tuesday’s better-than-expected JOLTS and Wednesday’s below-expectations ADP data.

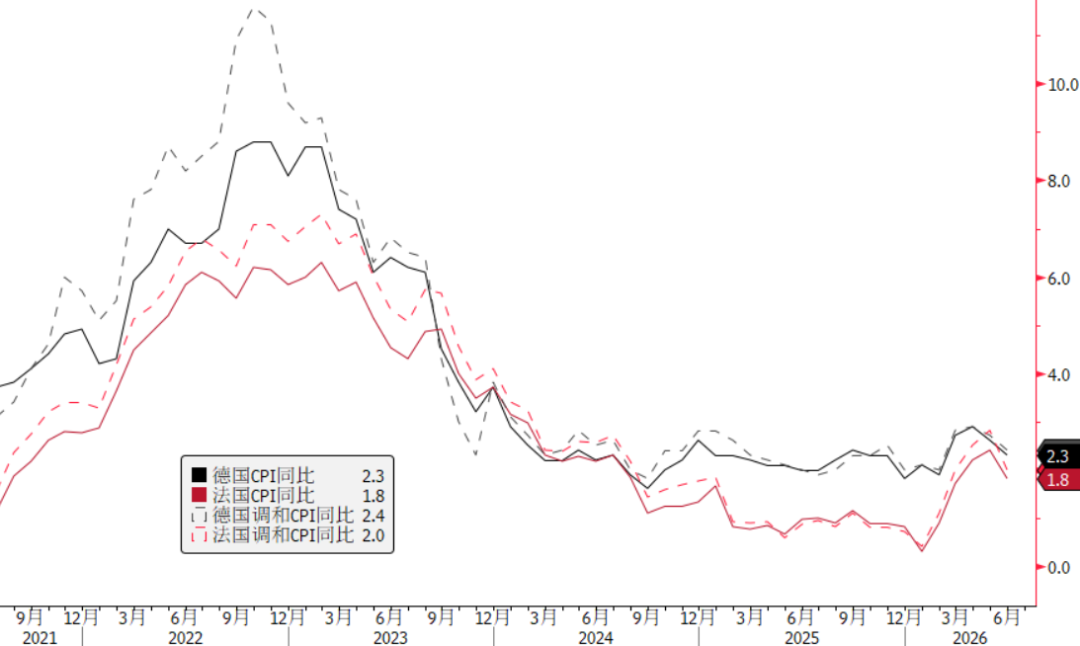

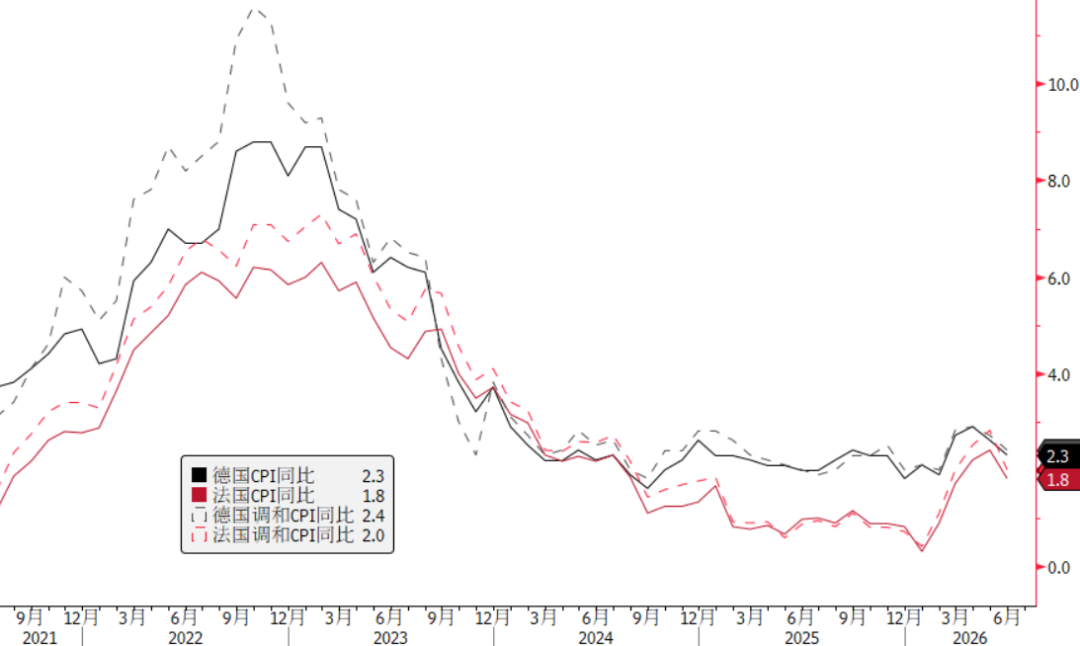

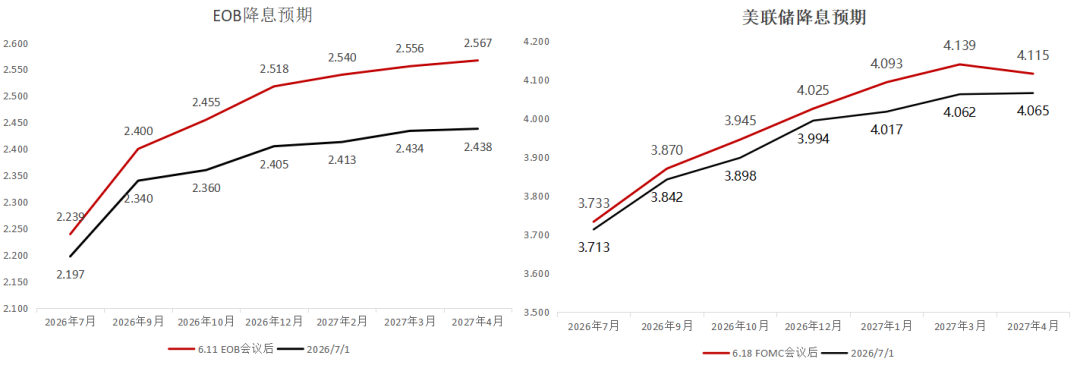

At the same time, the outlook in Europe is far from optimistic. German and French CPI data released on Tuesday and the Eurozone CPI released yesterday all fell short of expectations. The impact of the decline in oil prices in June has become apparent quickly, and expectations for ECB rate hikes this year have declined from 37bp after the June 11 meeting to 22bp.

2. U.S. Dollar Index gains lack momentum, what is the market hesitating about?

-

As we mentioned before regarding the crowded long position in the U.S. dollar, the current dollar bull position is quite crowded. For the dollar index to continue rising, the market’s bullishness on the dollar would have to be stronger than at any point in the past decade. From this perspective, the dollar index will likely oscillate below the 102 resistance; but if it breaks above 102 and long positions hit record levels, a substantial rally could occur.

-

The fall in European CPI may not be an isolated incident; with the sharp drop in oil prices in June, global CPIs may have already passed their peak and begun to decline. If this trend also appears in the U.S. CPI data on July 14, U.S. interest rates could fall, interest rate differentials with non-U.S. currencies may narrow, and this might drive the dollar index lower.

3. Can Nonfarm Payrolls push the Dollar Index above 102?

-

Scenario 1 (20%): Nonfarm payroll data significantly exceeds expectations, especially if wage growth is above forecast. This is the scenario most likely to lift U.S. rates and the dollar index. However, due to the “spoilers” from the White House, market expectations have been raised, so it may require nonfarm payrolls to increase by over 200,000 (expectation: 110,000), unemployment rate to be stable or lower, and monthly wage growth above 0.4% to drive a breakout in the dollar index.

-

Scenario 2 (70%): Nonfarm payrolls come in only slightly better than expected or match expectations. The market will not react strongly, and the dollar index will continue to oscillate below 102.

-

Scenario 3 (10%): Nonfarm payrolls miss expectations. Considering both Hassett and Boushey have said the data won’t disappoint, this outcome is very unlikely. If it happens, it not only means the U.S. economy is not as strong as thought, but also calls into question the credibility of White House officials. This could deal a second blow to dollar credibility, potentially pushing the index down to around 100.

[June U.S. Nonfarm Payrolls Prediction Game]

Prediction target: The number of new U.S. nonfarm payrolls in June (market expectation: 110,000; previous value: 172,000). Leave your prediction in the comments section. The 5 participants whose predictions are closest to the actual value will receive a Morning FX-branded T-shirt, and those ranking 6th to 10th will receive a branded canvas bag. Go to the comments section and leave your guess!

Source: Original Article

{kind=link}