US manufacturing is booming, but an inflation melt-up makes that look more like overheating than healthy growth. Will the stock market notice?

- US stocks ground higher as the S&P 500 hit another record on fading volume and weakening momentum

- ISM manufacturing PMI surged to its strongest since 2022, alongside a post-COVID-scale inflation spike

- Will ISM services PMI and US jobs data force equities to confront the same headwinds other markets fear?

Stock markets seem to have forgotten they used to care about crude oil. Prices jumped again today as a deal over the Strait of Hormuz remained elusive, yet Wall Street shrugged. The bellwether S&P 500 ground out yet another record high while every other major market kept pricing the inflationary fallout from the US-Iran war. The disconnect is now weeks old — and a busy macro calendar may finally test how long it can last.

Stocks stand alone as the war trade rolls on

The grind higher in stocks has the hallmarks of exhaustion. Gains have come on steadily diminishing volume — now fading sharply on the most recent leg higher — and the relative strength index (RSI) is flashing negative divergence, setting lower momentum readings even as price sets higher highs. That is not an outright topping signal, but it suggests the trend is losing steam. The level to watch is former resistance turned support just above 7500 – a break back below that may mark a genuine change of character.

Everywhere else, the “Iran war trade” rolls on. Crude oil bounced off what has become a wartime floor near $80 to $85 a barrel for West Texas Intermediate (WTI), rejecting weekend hopes of a 60-day ceasefire extension that never materialized as Washington and Tehran dug into their red lines. Treasury bond prices kept sliding. Gold continued its slow drip lower and the US dollar hugged the top of its range. These markets are telling the same story: a wartime energy price shock has evolved into a lasting inflation risk and beckons higher rates. Only stocks seem disinterested.

The manufacturing “boom” is really an overheating signal

Today’s macro data appeared to hand the bulls a gift. The Institute for Supply Management (ISM) manufacturing index surged to its strongest level since mid-2022. The final revision of the S&P Global manufacturing purchasing managers index (PMI) confirmed much of the same. On its surface, that looks like robust growth. The worrying part is what sits underneath.

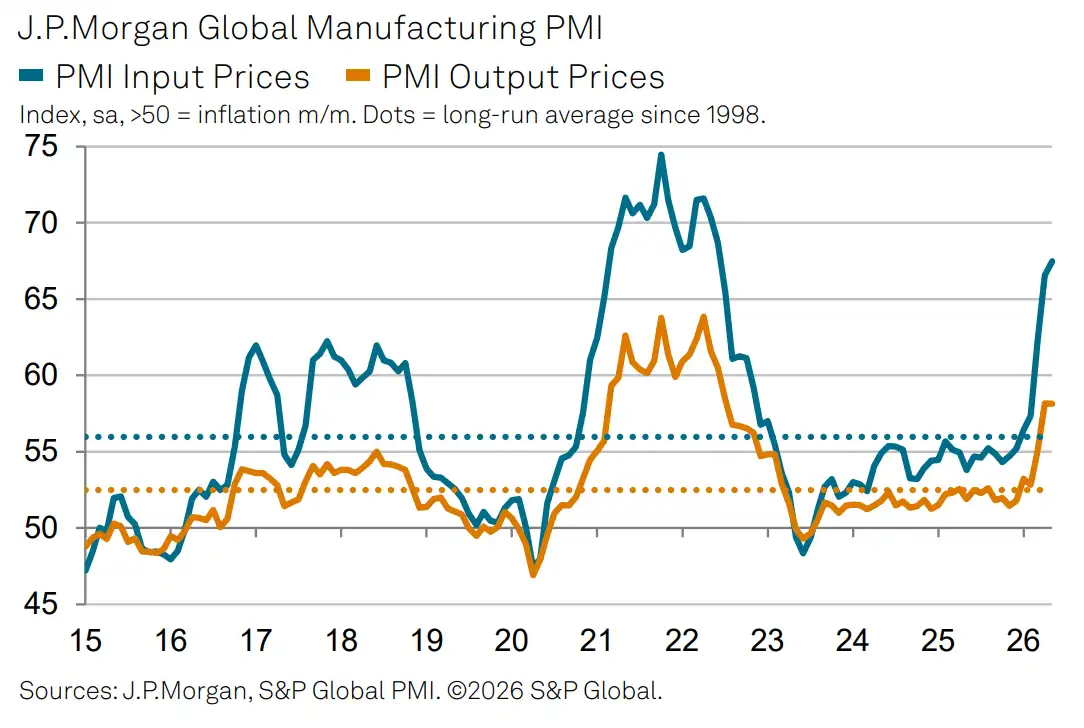

Much of the surge reflects stockpiling of inputs rather than end demand — manufacturers front-running an expected long pipeline of AI data center construction, tariff uncertainty after recent legal challenges, and the supply disruptions flowing from the closed Strait of Hormuz. Alongside it, the surveys show an inflationary melt-up to rival the post-COVID-19 pandemic peak. That earlier episode was the architecture for the aggressive 2022 rate-hike cycle that sent stocks lower all year. The JPMorgan global manufacturing PMI tells the same story worldwide: input and output prices running far above their long-run averages. This looks more like the profile of an economy overheating, not one that is growing in a healthy and sustainable way.

Last week’s downward revision to first-quarter US gross domestic product (GDP) data — cut to 1.6% from 2% annualized growth — reinforces the point. The markdown came almost entirely from softer consumer spending and business investment, the two essential engines of the economy. Consumption, 68% of GDP, was already contributing less to growth than fixed nonresidential investment at just 14%, thanks to the AI buildout. But both were revised down. Consumers are hamstrung by higher energy, higher input costs, and dearer credit — and so are the data center builders.

This week’s data will test the disconnect

Two tests stand out on a busy calendar. The ISM services PMI survey lands Wednesday. Compared with manufacturing, the sector drives a larger share of US employment and output. Recent consumer and producer price data have shown the energy shock already seeping into service-sector costs. Consensus looks for a relatively steady headline reading, but traders will comb through what lurks below the surface to gauge the inflationary threat.

The week closes with the US jobs report on Friday. Forecasts call for a rise of 96,000 in nonfarm payrolls for May, the smallest in three months, with the unemployment rate seen holding at 4.3%. A soft print would speak to gathering headwinds menacing the economy just as borrowing costs climb.

How long can stocks look the other way?

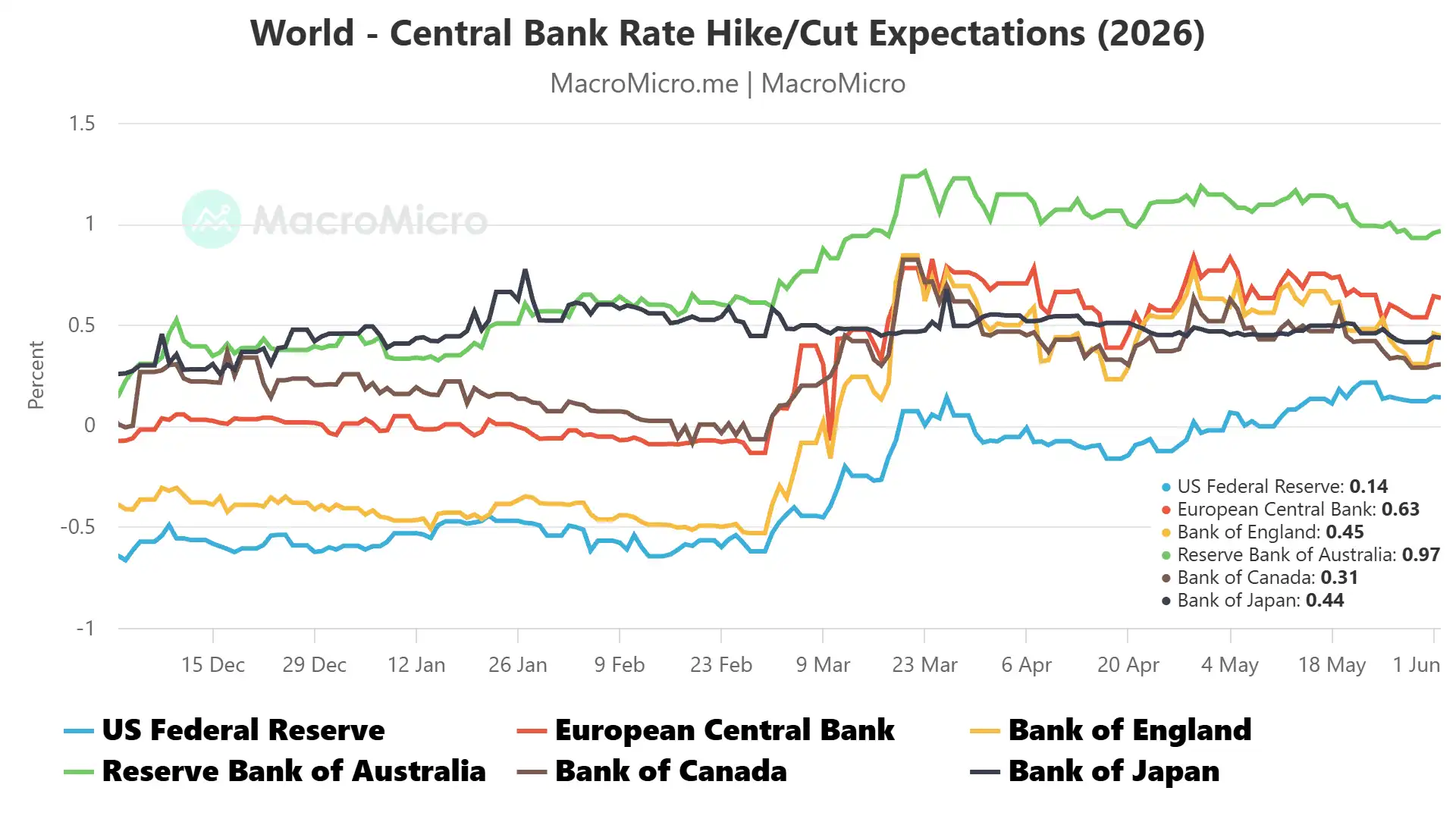

The bond market’s inflation expectations — the breakeven rates derived from the gap between nominal and inflation-protected yields — remain locked in step with crude oil and stuck near recent highs. The implication for policy is unambiguous: Fed funds futures now price about a 68% chance of a Federal Reserve rate hike this year, a stunning reversal from the 50 basis points (bps) of cuts the market expected before the war. The outlook for nearly every other major central bank has shifted to a more hawkish view in tandem.

That leaves equities on an island. The narrow rally has run on fading volume and ebbing momentum, sustained by an AI buildout story that the manufacturing data now reframes as part of the very inflation problem other markets are pricing. If service-sector ISM data confirms that cost pressure is spreading into the bulk of the economy, and Friday’s payrolls reveal a softening labor market, the case for a 14% slice of GDP to keep outpacing a hamstrung 68% slice grows thinner still. Stocks have ignored the message for weeks. The longer the disconnect persists, the more violent the reckoning is likely to be when it finally arrives.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

{kind=link}