How will the mega-IPOs affect market complexion? We’ve received many permutations of this question, with SpaceX having filed for its IPO and other unicorns like Anthropic and OpenAI waiting in the wings. Undoubtedly, concerns about market concentration—at both the stock and sector level—are behind some of these queries.

Thankfully, my Morningstar Indexes colleagues Alex Poukchanski and Alex Bryan (hereafter referred to as “the Alexes”) have published a paper on this topic. They focused on how SpaceX and other mega-IPOs will be handled by CRSP Market Indexes, a family of comprehensive equity benchmarks that came over to Morningstar as a result of our February acquisition of the Center for Research in Security Prices (CRSP), a former affiliate of the University of Chicago.

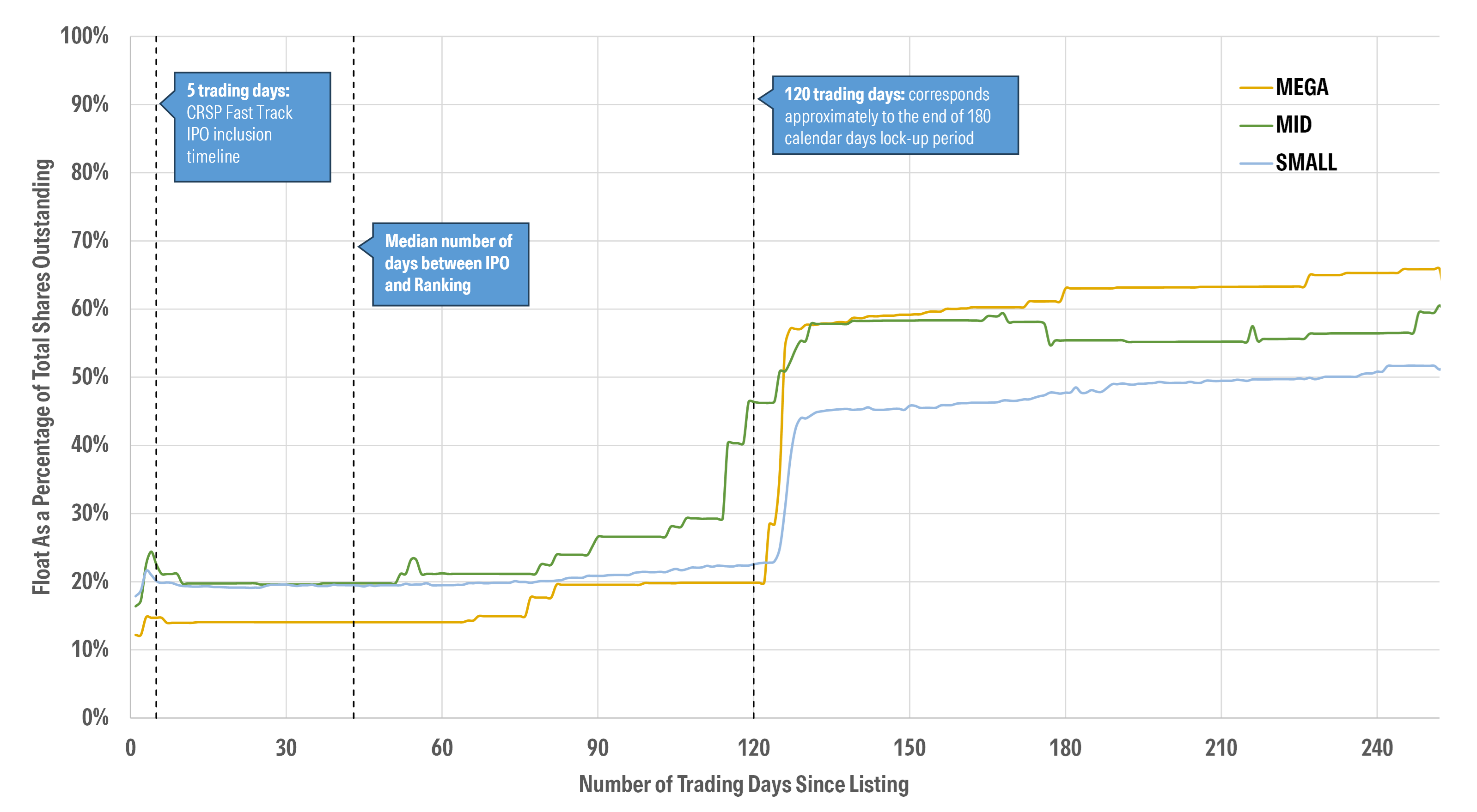

The Alexes’ paper contemplates the market impact of the mega-IPOs, both immediately after initial listing and then in the intermediate term. This phased analysis is important. Wonky terms like “free float” and “lockup periods” are key to understanding index inclusion, and, ultimately, how these newly public companies will change the stock market’s complexion.

The Initial Impact of the Mega-IPOs Will Be Muted

According to PitchBook, Morningstar’s private markets research arm, SpaceX is currently valued at $1.75 trillion. Not only does the company develop rockets and spacecraft, but it has acquired xAI, also founded by Elon Musk, putting it at the center of several mega-trends. A $1.75 trillion market cap would put it in the top 10 of the CRSP US Total Market Index.

But SpaceX will not be floating anywhere near its entire value to public market investors. Its IPO, expected to take place on June 12, 2026, will likely be for $75 billion, less than 5% of that $1.75 trillion valuation. Other potential mega-IPOs, including OpenAI, Anthropic, Stripe, and Databricks, will similarly list only a fraction of their values to public investors.

Like most index providers, CRSP uses a float adjustment when weighting stocks. Index constituent size is determined by market capitalization adjusted by free float. That adjustment reflects the piece of the pie available to investors.

The Alexes estimate initial weights for the mega-IPOs in CRSP market indexes based on their float-adjusted market capitalization. The impact is smallest in the total market index but greater for both the CRSP US Large Cap Index and the CRSP US Mega Cap Index. At a $75 billion float-adjusted market capitalization, SpaceX would receive a 12-basis-point (0.12%) weight in the total market index, falling well outside the top 100 constituents. (As weights adjust and constituents are reshuffled, indexes will experience some turnover, which is quantified in the paper.)

When it comes to classifying whether a stock is a mega-cap, large-cap, mid-cap, or small-cap, though, CRSP does not float adjust. Instead, it considers the value of total outstanding shares. When the CRSP size indexes undergo their scheduled reconstitution in June, they will reset their membership and rebalance their weights using total outstanding share-based market capitalization. Assuming current valuations, SpaceX, Anthropic, and OpenAI would rank among the top 25 stocks by this metric if they were public. They would be included in the mega-cap index and would displace other stocks, with cascading effects across size indexes.

Potentially Larger Impact on the Market Down the Road

We don’t know where share prices will go after the companies go public. But we do know that lockup periods restricting insider selling will expire, making more shares available in the market, and thereby increasing free float. Lockup periods typically end 120 trading days after the IPO, which corresponds to 180 calendar days. (SpaceX announced it will pursue a staggered lockup period, allowing for some earlier selling.)

Note: Mega, Mid, and Small refer to the CRSP capitalization categories (see Appendix for the definitions of the cap segments); IPOs are assigned to the capitalization categories based on the total shares outstanding capitalization using the closing price on the first day; Float shares are defined as the number of shares of a security outstanding that are freely available for trading by the public.

By the end of the lockup period, it’s typical for a company’s free float to rise to 50% to 60% of its overall value. As the float increases, so will the stock’s weighting in the indexes. CRSP US Market Indexes will implement float adjustments following the expiration of the lockup period at the first quarterly reconstitution after the end of the 180-day period. Assuming SpaceX’s valuation remains $1.75 trillion, that would make its float-adjusted market capitalization $875 billion, giving it a 1.33% weight in the CRSP US Total Market Index and larger weights in the large-cap and mega-cap indexes.

Mega-IPOs: What About Sector Impact?

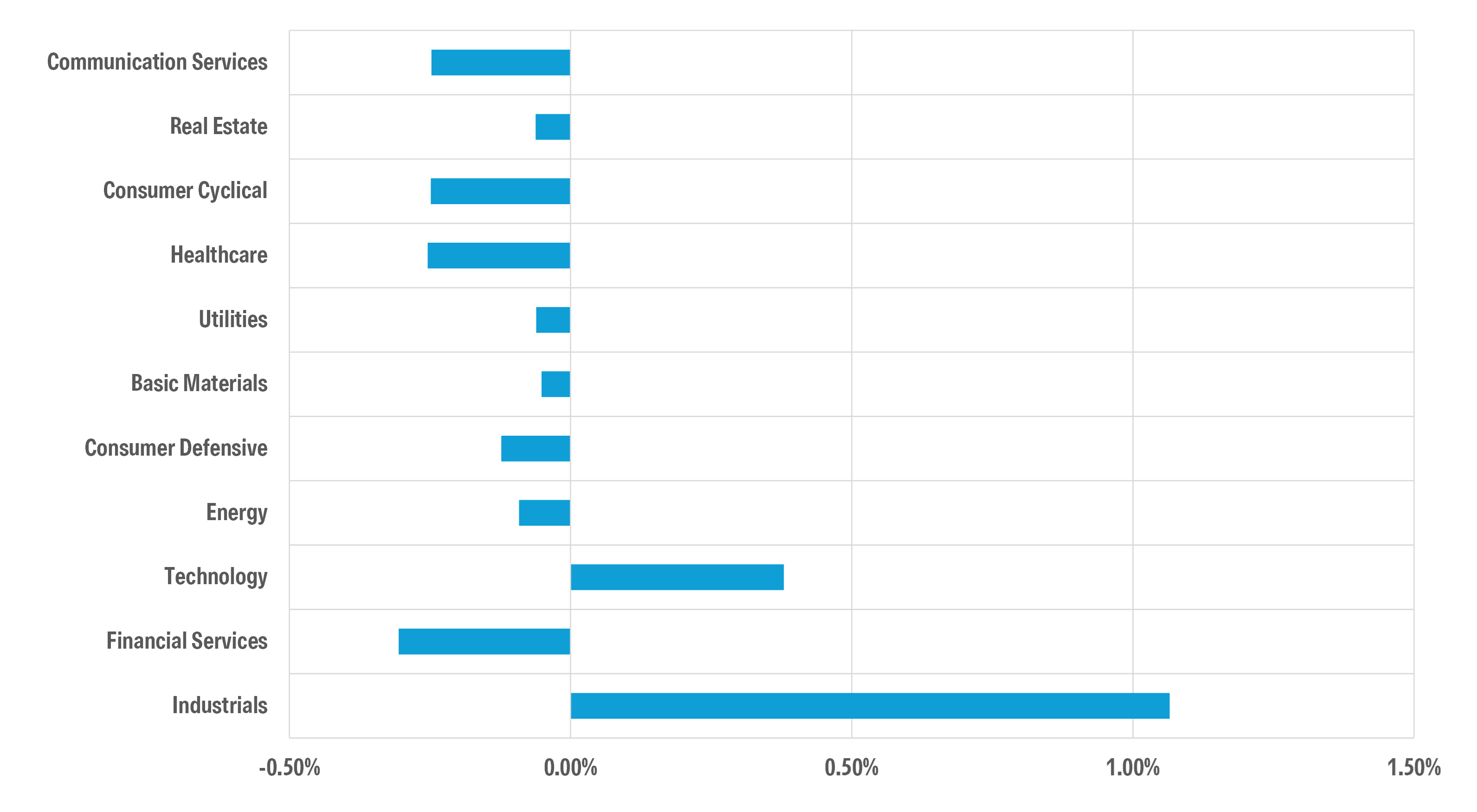

SpaceX will be classified in the industrials sector. OpenAI, Anthropic, Stripe, and Databricks are technology companies. Assuming free float eventually rising to 50% of current valuations, the new entrants will increase the CRSP US Total Market Index’s industrials weight by 1.1 percentage points and its technology sector weight by 0.4 percentage points.

Note: Except for SpaceX, valuations are based on PitchBook valuation estimates; float-adjusted capitalization is computed under the assumption of 50% float; SpaceX valuation is based on the reports in financial press; sector weights are computed based on Morningstar GECS methodology; overall impact shows the changes in sector allocations if all Mega-IPOs are included at the same time and at their current valuations and 50% float.

That’s not dramatic, but it does bump up the already high technology share of the CRSP US Total Market Index. The index’s technology weight stood at 33.5% as of April 30. Just five years ago, technology stocks represented 22.5% of the US stock market.

Mega-IPOs will have a bigger impact on sector indexes. Interestingly, new entrants to the technology sector would dilute the dominance of the largest companies, Nvidia NVDA, Apple AAPL, and Microsoft MSFT. This could make technology sector funds slightly more diversified at the stock level.

Adapting Index Rules for Changing Times

Like many index providers, CRSP has adjusted rules for the mega-IPOs. CRSP has long fast-tracked IPOs for benchmark inclusion to reflect the market in an up-to-date fashion. Since 2017, CRSP indexes have included newly public companies on the fifth trading day after listing. It is now relaxing requirements on the percentage of a company that must float publicly, given the size of upcoming IPOs.

“Recent changes to the float requirements reflect the fundamental challenges to the IPO universe, where companies are larger, and the offered float is often significantly lower than historical norms,” write the Alexes. Companies are staying private longer and achieving massive scale before publicly listing their shares. The mega-IPOs will change the face of the US stock market. But change won’t be sweeping and won’t come all at once.

Morningstar, Inc., licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. A list of ETFs that track a Morningstar index is available via the Capabilities section at indexes.morningstar.com. A list of other investable products linked to a Morningstar index is available upon request. Morningstar, Inc., does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

{kind=link}