- In late June 2026, Otter Tail Corporation (NasdaqGS: OTTR) was removed from multiple Russell growth benchmarks, including the Russell 3000 Growth, Russell 2000 Growth, and related extended and small-cap growth indices.

- This broad index removal matters because it can influence how index-tracking funds and growth-focused investors view Otter Tail’s role in diversified portfolios.

- Next, we’ll examine how Otter Tail’s removal from several Russell growth indices could influence the company’s existing investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

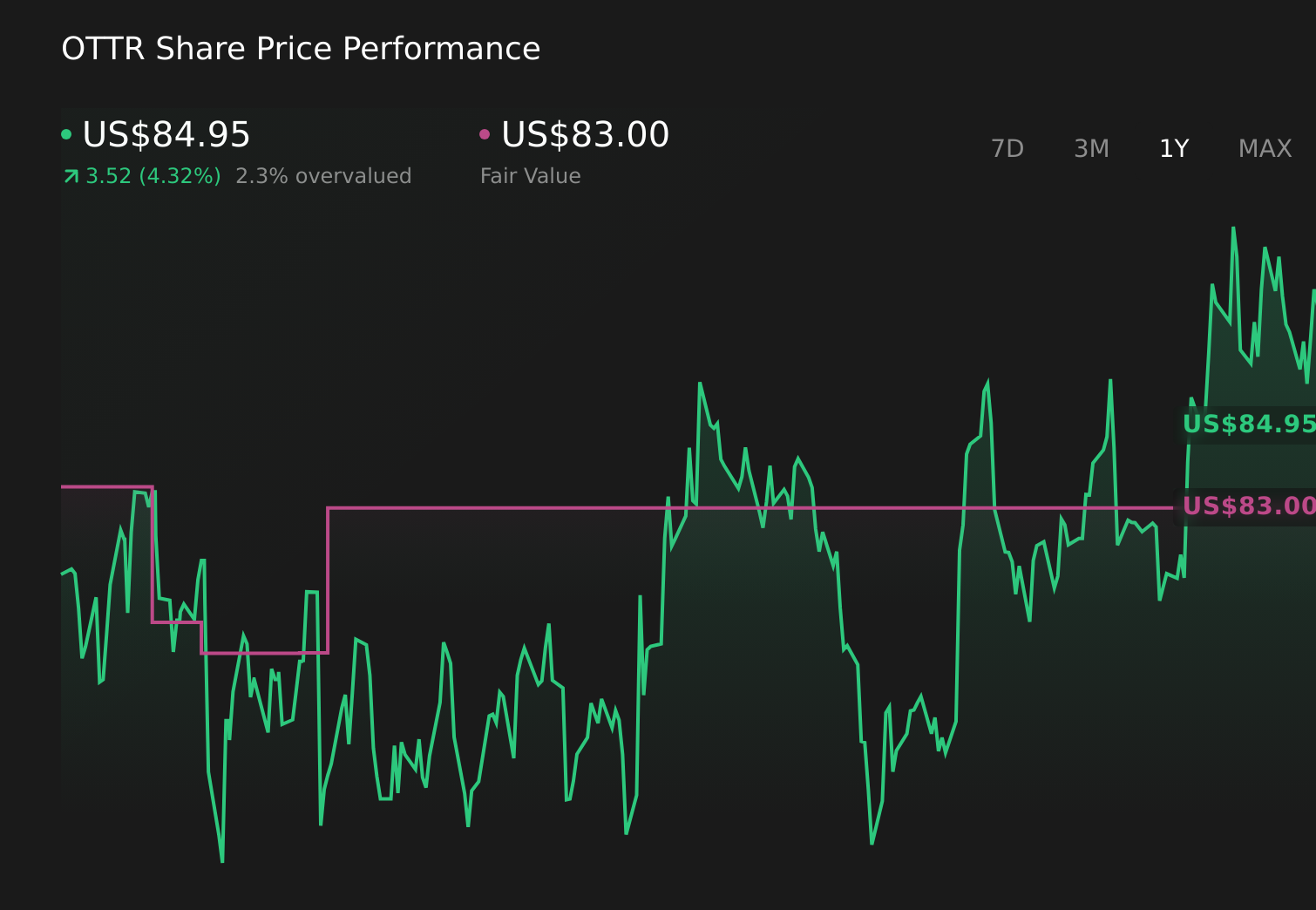

Otter Tail Investment Narrative Recap

To own Otter Tail, you need to be comfortable with a regulated utility and industrial portfolio where the core appeal is steady cash generation and a long record of dividends, not rapid growth. Its removal from several Russell growth indices is more about style classification than fundamentals, so it is unlikely to change the near term focus on execution in Utilities and Plastics or the key risk around earnings pressure and higher leverage.

The most directly relevant recent development is Otter Tail’s reaffirmation of its 2026 diluted EPS guidance of US$5.22 to US$5.62, issued in early May. That confirmation, together with ongoing capital investment plans in the utility segment, gives investors a reference point to judge how index exclusion interacts with expectations for slower forecast earnings and revenue growth and whether the current diversified model still supports the existing investment case.

Yet behind the stability story, investors should be aware of the ongoing PVC pipe antitrust settlements and what they could imply for…

Read the full narrative on Otter Tail (it’s free!)

Otter Tail’s narrative projects $1.4 billion in revenue and $206.7 million in earnings by 2029.

Uncover how Otter Tail’s forecasts yield a $90.50 fair value, in line with its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$72 to US$90 per share, underscoring how far apart individual views can be. Set against this, Otter Tail’s slower forecast earnings growth and higher debt levels may prompt you to weigh these differing opinions carefully and explore several alternative viewpoints before forming your own stance.

Explore 2 other fair value estimates on Otter Tail – why the stock might be worth 20% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}