- In late June 2026, Teradyne, Inc. was removed from several Russell value and defensive indices and added to growth-oriented benchmarks including the Russell 1000 Growth, Russell Midcap Growth, and Russell 3000 Growth indices.

- This reclassification signals that index providers now view Teradyne more as a growth company tied to AI-focused semiconductor testing and automation than as a traditional value stock.

- We’ll now examine how Teradyne’s shift into growth-focused Russell indices could reshape its AI-centered investment narrative for investors.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Teradyne Investment Narrative Recap

To own Teradyne, you need to believe in the long term demand for AI centric semiconductor testing and automation, despite cyclical swings and geopolitical noise. The key short term catalyst remains execution on AI data center test solutions, while the biggest current risk is exposure to tariffs and shifting trade policies that could unsettle customer spending. The Russell reclassification itself does not materially change these business drivers, but it may sharpen the focus on growth expectations and volatility.

The recent launch of Teradyne’s integrated AI test cell with Tokyo Electron is especially relevant here, because it directly supports the growth narrative underlying its move into Russell growth indices. By offering production ready screening for advanced AI and data center chips, this partnership sits at the center of Teradyne’s AI accelerator opportunity, and may influence how investors weigh the upside from new test platforms against ongoing risks in robotics, tariffs, and product mix.

Yet in contrast, investors should be aware that Teradyne’s concentration in cyclical, capex driven semiconductor markets could…

Read the full narrative on Teradyne (it’s free!)

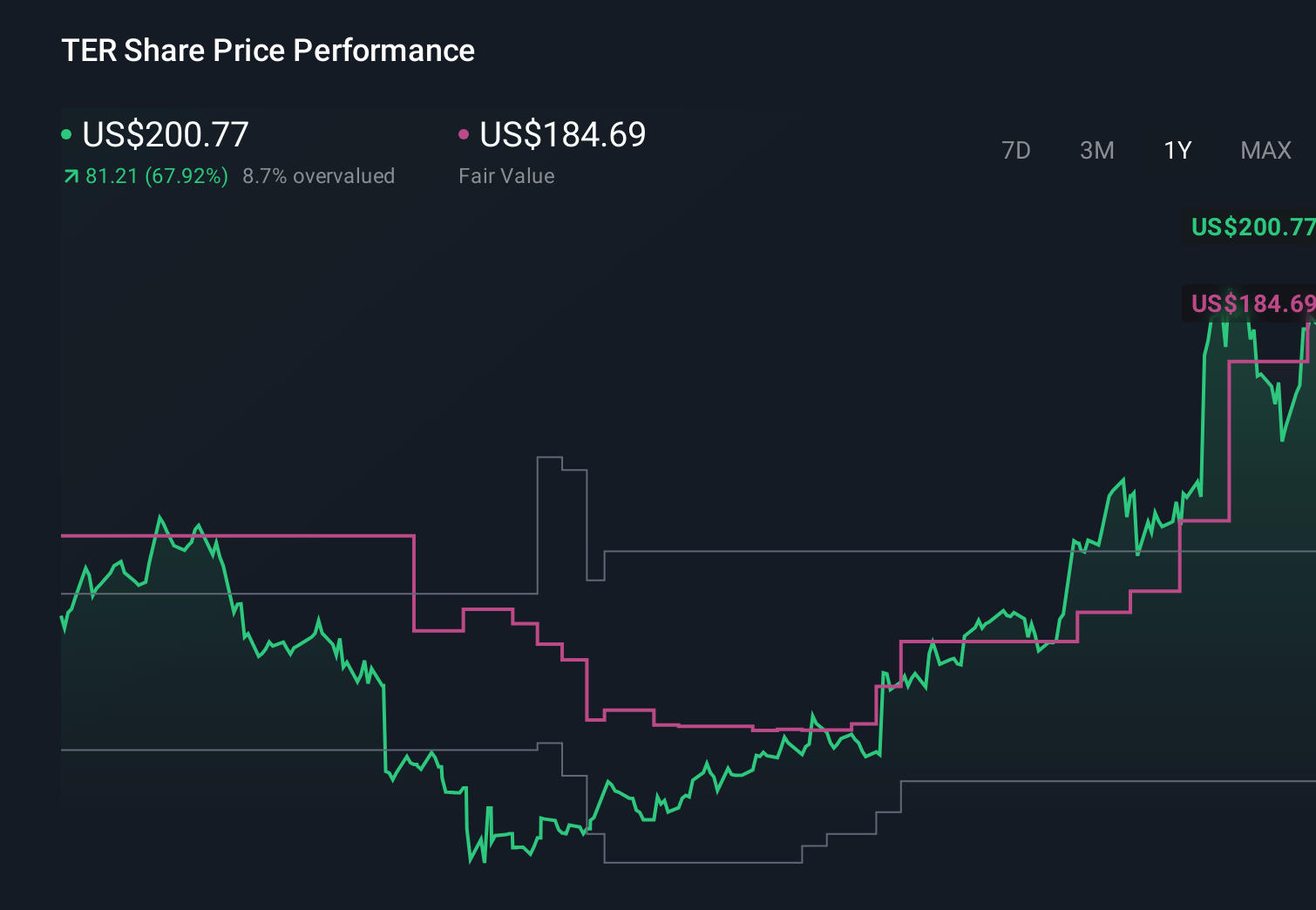

Teradyne’s narrative projects $7.0 billion revenue and $2.1 billion earnings by 2029. This requires 22.9% yearly revenue growth and about a $1.2 billion earnings increase from $854.1 million today.

Uncover how Teradyne’s forecasts yield a $416.65 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$8.6 billion and earnings US$2.9 billion, which is far above consensus, so you should expect that views on Teradyne’s AI test cycle and customer concentration risk might shift again as this index reclassification and related news are fully digested.

Explore 5 other fair value estimates on Teradyne – why the stock might be worth as much as 30% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Teradyne might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}