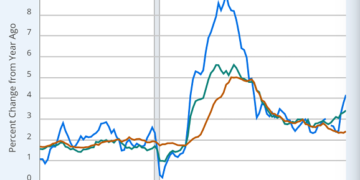

Cooling U.S. jobs data, softer expectations for Federal Reserve rate hikes, a weaker dollar and firmer gold prices are reshaping where risk and opportunity sit in the market. When rate expectations shift, capital often moves quickly between cash, bonds, stocks and real assets. This article looks at how that backdrop could affect specific companies tied closely to gold and precious metals, where revenues can be very sensitive to bullion prices and investor risk appetite. Below, you will find 3 stocks from the Gold and Precious Metals Stocks With Rate Shift Tailwinds screener that stand out as potential ideas for investors to research further in light of the latest macro developments.

Newmont (NEM)

Overview: Newmont is a large global miner that primarily produces gold, while also exploring for and producing copper, silver, lead, zinc and other metals across operations spanning the U.S., Latin America, Canada, Australia, Africa and Papua New Guinea.

Operations: Newmont generates revenue across a broad portfolio of mines, with key contributors including NGM (US$4.1b), Peñasquito (US$3.8b), Cadia (US$2.5b), Boddington (US$2.3b), Ahafo South (US$2.3b), Yanacocha (US$2.2b) and Lihir (US$2.1b), plus several mid sized assets.

Market Cap: US$99.2b

Newmont provides direct exposure to gold prices at a time when softer U.S. jobs data, lower Fed hike expectations and a weaker dollar have pushed bullion higher. The company is pairing that backdrop with high current profit margins, strong Return on Equity and a large global mine portfolio. Recent regulatory approvals to extend the life of the Red Chris operation and a sizeable buyback program sit alongside management’s ongoing focus on cost control, but investors also need to weigh operational risks at key assets and the complexity of integrating acquired mines and new leadership. For anyone following gold’s move and looking at large producers, Newmont’s mix of scale, earnings profile and project pipeline may warrant close attention.

Newmont’s scale and mine portfolio can make the headline story look simple, but the real edge may lie in how its earnings profile compares with that exposure. Review the DCF valuation analysis for Newmont.

SPDR Gold Shares (GLD)

Overview: SPDR Gold Shares (GLD) is a U.S. based exchange traded fund that holds physical gold and is designed to closely track the price of gold bullion, giving investors a way to access gold exposure through a stock market listing instead of buying and storing bars or coins themselves.

Market Cap: US$134.3b

SPDR Gold Shares sits at the intersection of the latest macro shifts and gold’s renewed appeal, since the ETF is built to mirror bullion prices and can see flows respond quickly when investors reassess interest rates, the dollar and inflation. GLD’s recent earnings profile, including 91.6% earnings growth over the past year and a high 30.7% Return on Equity, indicates a structure that has been very efficient at turning its gold exposure into returns for holders, even as reported revenues sit near zero and earnings are heavily non cash. At the same time, 100% reliance on external borrowings for liabilities and gaps in governance data introduce questions around risk. This makes it important to understand the mechanics behind those headline figures before deciding how GLD fits in a portfolio tied to gold and precious metals.

GLD’s earnings growth and high 30.7% Return on Equity hint at more going on beneath the surface than simple bullion tracking, and the full analysis report for SPDR Gold Shares could reveal what is really driving that profile

Franco-Nevada (TSX:FNV)

Overview: Franco-Nevada is a Toronto based royalty and streaming company that finances mines in exchange for a share of production. This gives it exposure to gold, silver, platinum group metals and some energy output without directly operating the mines.

Operations: Franco-Nevada generates most of its revenue from Precious Metals at about US$1.8b, with smaller contributions from Energy at roughly US$205m and Other Mining at about US$63m, alongside reported segment adjustments.

Market Cap: CA$57.3b

Franco-Nevada stands out in this rate shift and stronger gold backdrop because its royalty model links it tightly to bullion prices while limiting direct operating and cost inflation risks, and its high 65.7% net margins and solid 16.9% Return on Equity underline that efficiency. Forecast double digit earnings and revenue growth ahead of the Canadian market, a strong balance sheet and record royalty income give it capacity to pursue new streams as producers look for funding. The flip side is meaningful exposure to a handful of large assets such as Cobre Panamá and Candelaria and ongoing legal and permitting disputes that can affect future cash flows. For investors weighing gold exposure without running a mine, Franco-Nevada’s mix of growth, income and concentration risk deserves closer scrutiny.

Franco-Nevada’s royalty engine appears positioned for accelerating earnings, but the real story may lie in how future deals reshape that growth path. Get the full analyst forecasts for Franco-Nevada and see what might shift next.

Take Control of Your Investment Journey

If Franco-Nevada or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Gold?

Some stocks are already building breakout momentum while others stay under the radar for now. Before prices start flying and the best entry points are gone, consider positioning earlier.

- Explore early growth stories with real balance sheet strength by scanning the curated 18 high quality undiscovered gems before the crowd notices what is quietly building momentum.

- Focus on resilient payers with yields that can matter when markets cool by reviewing a focused set of 7 dividend fortresses while the prices have not fully adjusted.

- Review companies at the core of potential future energy systems by checking a filtered group of 35 power grid technology and infrastructure stocks before the grid upgrade theme moves out of focus.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Newmont might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}