The upward movement in Lam Research is primarily driven by a broader rally in the semiconductor capital equipment sector. As leading chipmakers accelerate their transitions to next-generation architectures like Gate-All-Around transistors, the demand for high-precision etch and deposition tools has intensified. Lam Research, being a dominant player in these specific processes, is benefiting from increased capital expenditure budgets at major foundries and memory manufacturers. The market is increasingly pricing in the long-term necessity of the company’s specialized hardware for the production of advanced artificial intelligence hardware.

Renewed strength in the memory segment is acting as a significant catalyst for this price appreciation. After a period of inventory digestion, NAND and DRAM producers are shifting focus toward High-Bandwidth Memory to meet the requirements of high-performance computing. Lam Research’s high-aspect-ratio etching technology is critical for the vertical stacking required in these advanced memory configurations. Reports of capacity expansions by key clients in Asia have bolstered investor confidence, suggesting that shipment volumes may exceed previous conservative estimates for the upcoming fiscal periods.

Beyond industry-specific fundamentals, favorable macroeconomic conditions are providing a tailwind for growth-oriented technology stocks. Recent data indicating a stabilization in global manufacturing and a softening of inflationary pressures have led to a decrease in long-term bond yields, making high-multiple stocks more attractive to institutional investors. The significant intraday volatility suggests a contest between short-term profit-taking and long-term funds rebalancing their portfolios toward high-quality semiconductor names ahead of the core quarterly earnings cycle.

Positive commentary from several sell-side analysts has further fueled the momentum. Upgrades focusing on the resilience of the company’s service-based revenue, which provides a cushion against cyclical hardware fluctuations, have improved the overall risk-reward profile in the eyes of the market. While geopolitical tensions and export controls remain a persistent background risk, the current market sentiment is heavily focused on the immediate supply-demand imbalance for advanced wafer fabrication equipment. This optimism is reflected in the stock’s ability to outperform the broader market indices during the current session.

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of -18.049, indicating a neutral signal. The RSI at 44.983 suggests neutral condition and the Williams %R at 86.587 suggests oversold condition. Please monitor closely.

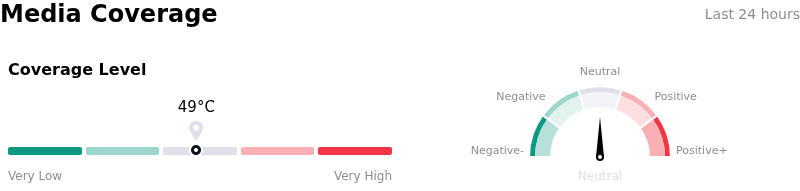

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $359.85, a high of $480.00, and a low of $213.00.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Source: Original Article

{kind=link}