Lam Research is experiencing notable downward pressure as the semiconductor equipment sector grapples with a confluence of macroeconomic and industry-specific challenges. The significant intraday volatility reflects a shift in investor sentiment, moving away from high-growth technology assets toward more defensive positions. This trend is driven by emerging data suggesting a potential slowdown in global industrial production, which directly impacts the demand for the advanced wafer fabrication equipment Lam provides.

A primary driver for the current weakness is the heightened geopolitical risk surrounding export regulations. As a dominant player in the etching and deposition space, the company is particularly vulnerable to any updates in trade policies that restrict the sale of sophisticated tools to major manufacturing hubs. Reports suggesting further limitations on equipment capable of producing advanced logic and memory chips have caused institutional investors to reassess the company’s revenue trajectory for the coming quarters.

Furthermore, the memory market cycle is showing signs of maturation. After a period of aggressive capacity expansion driven by artificial intelligence infrastructure, there are indications that major chipmakers are tightening their capital expenditure budgets. Lam Research, which maintains a heavy exposure to the NAND and DRAM segments, is seeing its valuation compressed as analysts project a cooling period for new tool orders. This cyclicality remains a persistent concern for shareholders, especially when coupled with rising operational costs.

From a market strategy perspective, the stock’s performance today is also influenced by broader sector rotation. As yields on government bonds fluctuate in response to the latest inflation data, high-multiple stocks like Lam Research often face valuation adjustments. The lack of a near-term catalyst, combined with downward revisions to earnings forecasts by several research firms, has removed the support levels that previously buoyed the share price, leading to the current decline.

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of -16.960, indicating a neutral signal. The RSI at 49.051 suggests neutral condition and the Williams %R at 70.311 suggests sell condition. Please monitor closely.

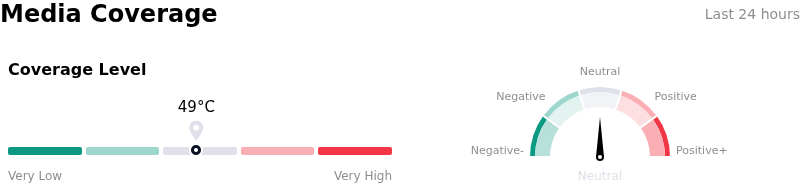

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $359.85, a high of $480.00, and a low of $213.00.

p>Company Specific Risks:

- Geopolitical Export Restrictions: Renewed speculation regarding tighter U.S. Department of Commerce controls on advanced etching technology has triggered intraday selling, as any expansion of the “Entity List” or licensing restrictions directly threatens Lam’s substantial revenue derived from Chinese semiconductor manufacturers.

- NAND Recovery Uncertainty: Institutional analysts have raised concerns that the anticipated rebound in NAND capital spending is losing momentum, potentially leading to a revenue shortfall for Lam in the coming quarters given its high sensitivity to memory industry cycles compared to diversified peers.

- Technological Transition Execution: Intraday volatility has increased following reports of yield hurdles in the transition to next-generation Gate-All-Around (GAA) architectures at key customer sites, which threatens to delay the procurement of Lam’s specialized deposition and etch toolsets.

- Operational Margin Pressures: Current market movement reflects anxiety over rising R&D expenditures and supply chain costs associated with developing 3D-DRAM solutions, which analysts fear will exert downward pressure on gross margins if high-volume production cycles are deferred.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Source: Original Article