- On 27 June 2026, Polaris Inc. (NYSE:PII) was reclassified within the Russell index family, moving out of multiple value benchmarks and into several growth and growth‑defensive indices, while also scheduling its second-quarter 2026 results release and earnings call for 28 July 2026.

- This broad shift from value-oriented to growth-focused benchmarks reshapes how Polaris is positioned in indexed portfolios and may influence how investors interpret its business profile and future potential.

- We’ll now explore how Polaris’s migration into growth-oriented Russell indices may affect the existing investment narrative built around tariffs and demand.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Polaris Investment Narrative Recap

To own Polaris today, you need to believe its premium brands, product pipeline, and dealer network can offset tariff uncertainty, soft powersports demand, and recent losses. The Russell reclassification toward growth indices does not change the near term focus on tariffs and end market demand, but it may shift which funds hold the stock and how investors frame the balance between risk and recovery potential.

The most relevant recent announcement here is Polaris scheduling its second quarter 2026 results and earnings call for 28 July 2026. With the stock now in growth focused Russell benchmarks, that update takes on added weight as investors look for signs that tariff mitigation, pricing, and new product launches are translating into better earnings quality and a path toward covering the dividend and improving the balance between growth ambitions and financial risk.

Yet behind the growth label, investors should be aware that prolonged tariff pressure and weaker retail demand could still…

Read the full narrative on Polaris (it’s free!)

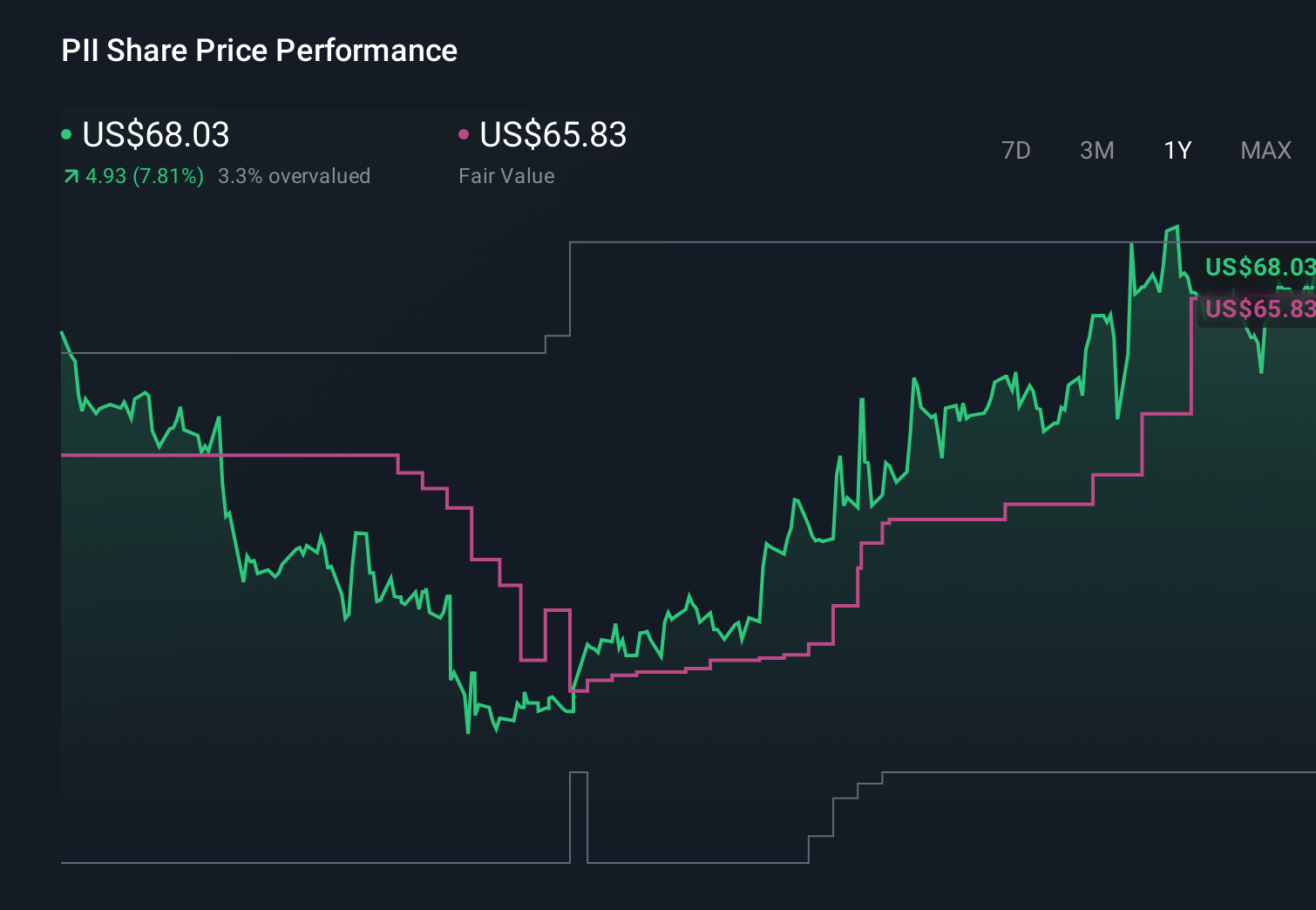

Polaris’ narrative projects $7.8 billion revenue and $425.0 million earnings by 2029. This requires 2.1% yearly revenue growth and about an $871 million earnings increase from -$446.1 million today.

Uncover how Polaris’ forecasts yield a $68.00 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue near US$8.1 billion and earnings above US$400 million, but the index move and ongoing electrification risks show how far opinions can differ and why you should weigh several views before deciding what this shift in growth expectations might really mean.

Explore 3 other fair value estimates on Polaris – why the stock might be worth 27% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Looking For Alternative Opportunities?

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}