Geopolitical tension in the Strait of Hormuz has once again put the spotlight on supply risk, shipping routes, and the cost of getting crude to market. For investors, that kind of disruption can quickly change expectations for producers’ revenues, capital plans, and risk profiles. This article looks at how the latest Iranian threats to shipping could affect selected oil and gas producers in our Energy Sector screener, and what that might mean for their risk and return trade offs. Three stocks that appear most exposed to this news driven theme, all on the positive side, are revealed in the sections that follow.

Viper Energy (VNOM)

Overview: Viper Energy is a US based company that owns and acquires mineral and royalty interests in oil and natural gas properties in the Permian Basin, collecting a share of production revenue without directly operating wells. Founded in 2013 and now a subsidiary of Diamondback Energy, it functions as a pure play on Permian drilling activity and commodity prices.

Operations: Viper Energy generates its entire US$1.6b in revenue from owning and acquiring mineral and royalty interests in the United States.

Market Cap: US$14.8b

Viper Energy provides exposure to Permian oil volumes and crude prices without the capital intensity of running rigs. This can be particularly relevant when shipping risks around the Strait of Hormuz affect global supply routes and pricing dynamics. The company is prioritizing scale through the Sitio Royalties acquisition and recent production guidance updates, and its dividend yield and inclusion in defensive indices indicate that income focused investors are paying attention. At the same time, Viper Energy is still working through losses, relies on third party operators and faces governance questions related to board turnover and pay. The long term opportunity is closely tied to how effectively it manages these financial and operational trade offs.

Viper Energy’s royalty model offers oil price exposure without heavy drilling spend, but the real story lies in how its cash flows compare with its current risks. To explore this further, start with the 3 key rewards and 2 important warning signs (1 is major!)

Meren Energy (TSX:MER)

Overview: Meren Energy is a Canadian oil and gas producer focused on exploration and production projects in Nigeria, Namibia, South Africa, and Equatorial Guinea, giving investors exposure to a portfolio of offshore African assets across both producing fields and longer dated developments.

Operations: Meren Energy generates approximately US$600 million in revenue from international oil and gas exploration activities.

Market Cap: CA$1.3b

Meren Energy may appeal to investors who want direct leverage to global oil prices at a time when shipping risks around the Strait of Hormuz are raising concern about future supply. The company combines producing Nigerian assets with large projects such as the Venus development in Namibia, while offering a double digit dividend yield and trading below some estimates of fair value. At the same time, Meren is loss making, highly dependent on external funding and long lead projects, and carries concentrated geopolitical risk in several African jurisdictions. For investors, the key consideration is whether that mix of income potential, discounted valuation, and execution risk aligns with their individual risk tolerance and objectives.

Meren Energy’s mix of high yield, offshore projects and concentrated country exposure can look like a puzzle that markets have not fully pieced together yet, and the 3 key rewards and 1 important warning sign could highlight the one pressure point that really matters.

Greenfire Resources (GFR)

Overview: Greenfire Resources is a Canadian oil and gas company focused on developing and operating its Hangingstone Facilities in the Athabasca oil sands region near Fort McMurray, giving investors exposure to thermal heavy oil production in Alberta.

Operations: Greenfire Resources generates approximately CA$550.6 million in revenue from its oil sands operations in Canada.

Market Cap: CA$703.7 million

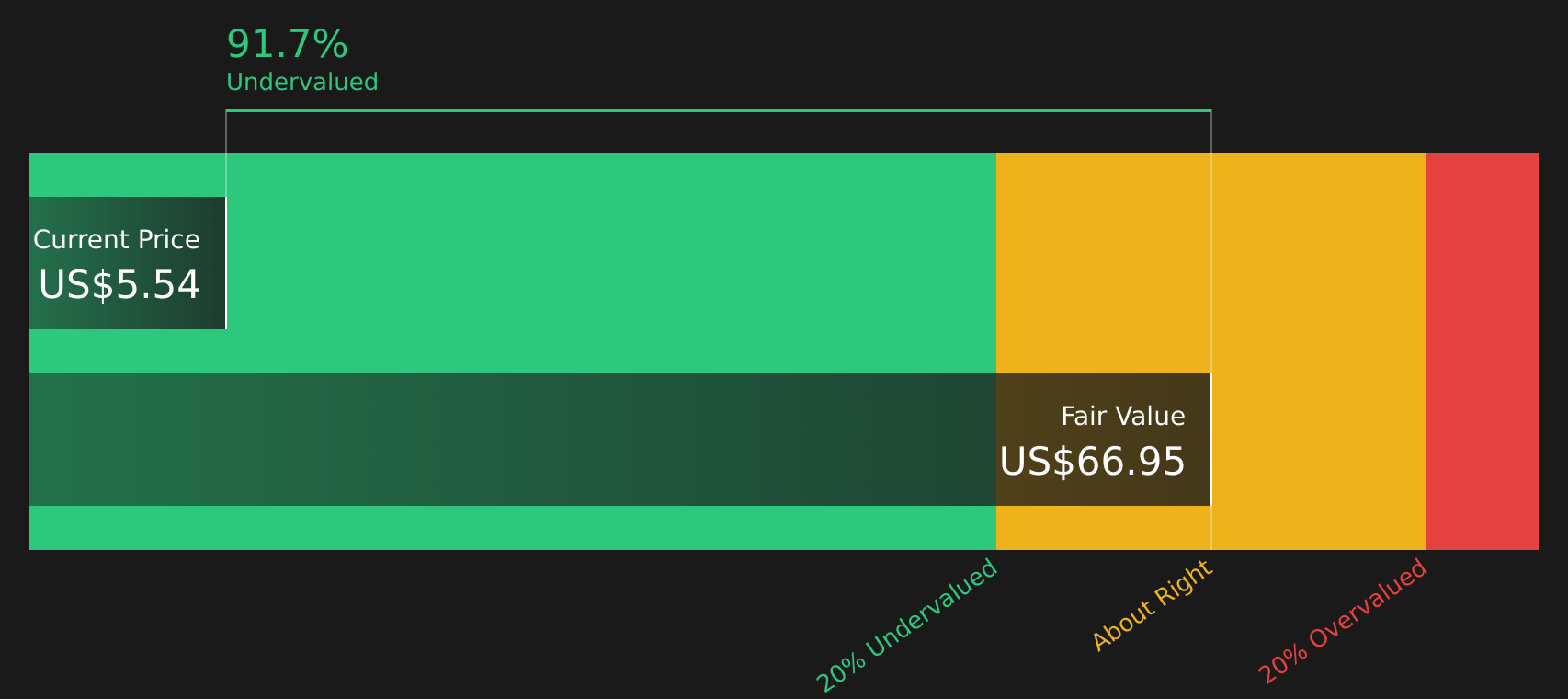

Greenfire Resources stands out as a pure play on Canadian oil sands at a time when threats around the Strait of Hormuz are keeping attention on supply risk and global oil pricing. The stock trades at a steep discount to some estimates of its fair value, yet the business is still loss making, with Return on Equity in decline and revenue growth forecast to trail both the broader market and peers. Add in a relatively new board and management team and you have meaningful execution and funding risk. The key question is whether that mix of discounted valuation, production guidance and higher oil price sensitivity compensates you for those pressures, especially with a major earnings date already on the calendar.

Greenfire Resources appears to be a valuation outlier, with oil sands exposure and loss making financials that do not fully line up on first glance. The analysis report for Greenfire Resources could reveal what the market might be missing next.

The three stocks in this article are only a starting point, and the full Energy Sector – Oil & Gas Producers screener surfaces 28 more producers with equally compelling narratives around scale, balance sheets and exposure to global crude markets. Use Simply Wall St to identify, filter and analyze the specific catalysts and storylines that matter to you so you can focus on the highest conviction opportunities in this part of the energy sector.

Take Control of Your Investment Journey

If Greenfire Resources or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point.

Once you’ve made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates.

Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives.

By uncovering hidden catalysts and risks early, you’ll accelerate your decision-making and stay one step ahead of the market.

Curious About Alternative Stock Paths?

Fresh ideas move fast, and the stocks with real breakout potential rarely stay under the radar for long. Scan these focused lists before the momentum is caught and consider acting while opportunities are still developing.

- Spot companies where strong balance sheets back the story by using a curated list of solid balance sheet and fundamentals (46 results) that filters for financial strength while it still flies under the radar for now.

- Explore structural shifts in computing by checking a hand picked group of 26 quantum computing stocks that could build momentum long before most investors pay attention.

- Target potential compounding machines early with a focused pool of 20 top founder-led companies before these stories move from quiet execution to headlines and rapidly changing entry points.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}