UPCOMING

EVENTS:

- Monday: New Zealand Services PMI, NY Fed Consumer Inflation

Expectations. - Tuesday: RBA Meeting Minutes, UK Employment Report, German

ZEW, Canada CPI. - Wednesday: Japan Tankan, China Industrial Production and

Retail Sales, UK CPI, US Retail Sales, US Industrial Production and

Capacity Utilisation, BoC Policy Announcement, US NAHB Housing Market

Index, Fed Chair Powell. - Thursday: New Zealand Q1 CPI, Australia Employment

report, ECB Policy Announcement, US Housing Starts and Building Permits,

US Jobless Claims. - Friday: Japan CPI (Good Friday Holiday)

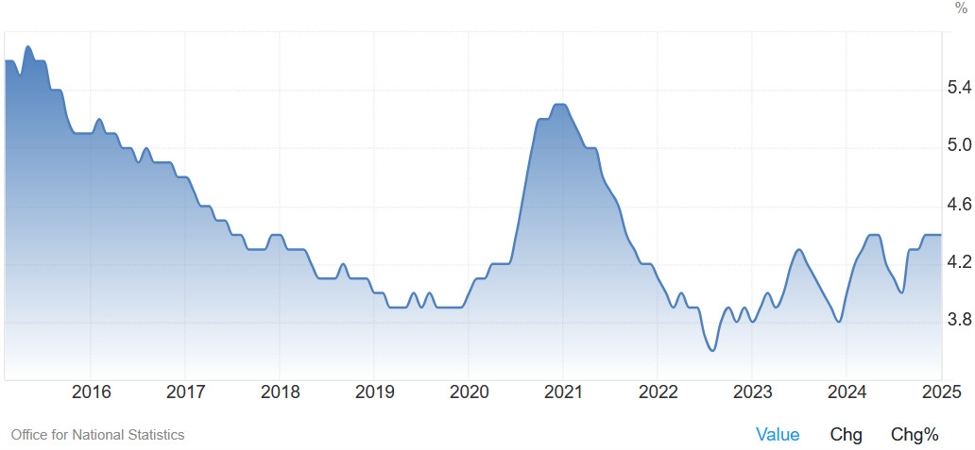

Tuesday

The UK

Unemployment Rate is expected to remain unchanged at 4.4%. The Average Earnings

are expected at 5.7% vs. 5.8% prior, while the Ex-Bonus Earnings are seen at 6.0%

vs. 5.9% prior. The data is unlikely to influence market expectations as the

focus remains on the tariff negotiations and the US-China developments. The

market is currently pricing 76 bps of easing by year-end with an 85%

probability of a 25 bps cut at the upcoming meeting.

UK Unemployment Rate

The Canadian CPI

Y/Y is expected at 2.6% vs. 2.6% prior, while the M/M reading is seen at 0.6%

vs. 1.1% prior. The Trimmed-Mean CPI Y/Y is expected at 3.0% vs. 2.9% prior,

while the Median CPI Y/Y is seen at 3.0% vs. 2.9% prior.

Inflation has been

moving higher recently after the aggressive BoC easing and the tariffs are

expected to keep inflation higher while weighing on growth. The market sees 36

bps of easing by year-end with a 61% probability that the central bank will

hold rates unchanged this week.

Canada Inflation Measures

Wednesday

The UK CPI Y/Y is

expected at 2.7% vs. 2.8% prior, while the M/M reading is seen at 0.4% vs. 0.4%

prior. The Core CPI Y/Y is expected at 3.5% vs. 3.5% prior, while Services CPI

Y/Y is seen at 4.9% vs. 5.0% prior.

Again, the data this

month is unlikely to influence market’s expectations that much as the focus

remains on tariff negotiations. The market is currently pricing 76 bps of

easing by year-end with an 85% probability of a 25 bps cut at the upcoming

meeting.

UK Core CPI YoY

The US Retail

Sales M/M is expected at 1.4% vs. 0.2% prior, while the ex-Autos figure is seen

at 0.4% vs. 0.3% prior. The focus will be on the Control Group figure which is

expected at 0.6% vs. 1.0% prior.

Consumer spending

has been stable in the past months which is something you would expect given

the positive real wage growth and resilient labour market. More recently

though, we’ve been seeing some marked easing in consumer sentiment due to the

ongoing trade wars which could weigh on spending going forward.

US Retail Sales YoY

The BoC is

expected to keep rates unchanged at 2.75%. As a reminder, the BoC cut interest

rates by 25 basis points to 2.75% as expected at the last meeting amid concerns

over weaker growth ahead due to the trade uncertainty and US tariffs. The

central bank emphasized a cautious approach to future decisions, balancing the

upward pressure on inflation against the downward pressure on weaker demand. The

market expects just one last cut by year-end.

Bank of Canada

Thursday

The New Zealand Q1

CPI Y/Y is expected at 2.3% vs. 2.2% prior, while the Q/Q figures is seen at

0.7 vs. 0.5% prior. The market sees 103 bps of easing by year-end with a 72%

probability of a 50 bps cut at the upcoming meeting. All these market

expectations about interest rates were influenced by the global market rout

following Trump’s aggressive tariffs. That’s where the focus is now. A reversal

or easing in the trade war would diminish the aggressive rate cuts

expectations.

New Zealand Q1 CPI YoY

The Australian

Employment report is expected to show 35K jobs added in March vs. -52.8K in February,

and the Unemployment Rate to tick higher to 4.2% vs. 4.1% prior. The US trade

war and the global market selloff pushed the market to expect 107 bps of easing

by year-end with a 40% probability of a 50 bps cut at the upcoming meeting.

Australia Unemployment Rate

The ECB is

expected to cut by 25 bps bringing the deposit rate to 2.25%. The market then

expects at least two more rate cuts by year-end. Interest rates expectations

have been shaped by the ongoing trade war and the recent 90-days pause for

reciprocal tariffs helped to alleviate the aggressive pricing. Again, it’s all

about the trade war now as the data remains old news.

European Central Bank

The US Jobless

Claims continue to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims hover

around cycle highs.

This week Initial

Claims are expected at 226K vs. 223K prior, while there’s no consensus for

Continuing Claims at the time of writing although the prior release saw a

decrease to 1850K vs. 1893K prior.

US Jobless Claims

Friday

The Japanese Core

CPI is expected at 3.2% vs. 3.0% prior. Given the global market rout and

aggressive risk off sentiment, traders scaled back their rate hikes

expectations and they now see the BoJ remaining on hold for the rest of the

year. Of course, this is all connected to the trade war so an easing and positive

developments on that front should increase the expectations for a rate hike by

year-end.

Japan Core CPI YoY

{kind=link}