Key Takeaways

- Economists forecast another solid month of hiring for June, though slower than the unexpectedly strong May pace.

- Leisure, hospitality, and other sectors could see softer hiring due to short-term employment trends that ended in May.

- Economists are divided on how the expected healthy jobs data will influence a Fed rate decision.

After three consecutive months of strong job gains, economists forecast the June employment report will show another healthy increase in hiring, albeit at a more moderate pace than in May.

Economists expect 100,000 new jobs in June, a nearly 72,000 drop from May, according to FactSet consensus estimates. The unemployment rate is forecast to remain unchanged at 4.3%. “Job growth has been quite strong. It has been very consistent with other strong data that we’ve been seeing across the economy,” says Vanguard Senior Economist Josh Hirt.

The strong reading is expected to spur the Federal Reserve to keep interest rates on hold for the time being, but economists are divided on whether it may hike rates later this year. The Fed is seen as more focused on inflation, which has been running above its target since 2021 and has been hot this year amid the Iran-war-driven spike in energy costs.

Over the past three months, job creation has aligned with broader positive economic data like GDP. However, some hiring trends have occurred earlier than expected this year, and technical adjustments may explain the softening pullback, which economists widely expected to begin in June. We may not see overly strong numbers compared with the past few months. “The interesting thing is why some of that strength was there, and that leads us into a cautious outlook—not just for Friday, but maybe over the next couple of months as well,” says Hirt.

May Jobs Report Forecast Highlights

- Job report release date and time: Thursday, July 2, at 8:30 a.m. EDT

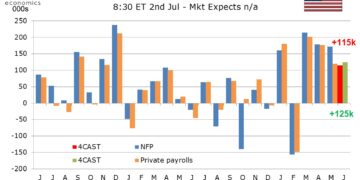

- Nonfarm payroll employment is forecast to increase by 100,000 in June vs. 172,000 in May, according to FactSet.

- The unemployment rate is forecast to remain at 4.3%.

- The average workweek is forecast to remain at 34.3.

- Hourly earnings are forecast to remain at 0.3%.

June Numbers to Show Pullback

The US economy has averaged job gains of more than 188,000 per month over the last three months, a significant pickup from weak readings across most of 2025 and into February of this year. Economists say this trend likely overstates the strength of hiring, but the job market would still be in good shape with a 100,000 increase in non-farm payrolls.

Bank of America economists forecast a “robust” 110,000 increase in a recent report. They point to “benign” weekly jobless claim readings and strong numbers from the monthly ADP report. “That said, we see downside risks: May’s surge in leisure & hospitality may have been driven by the World Cup or Memorial Day timing, and if it was the latter, June could see payback,” they wrote.

At JP Morgan, economists are calling for nonfarm payroll growth of 125,000 jobs, but they highlight areas of moderating gains. Local government jobs, which jumped 52,000 in May, also experienced temporary help from elections in only some states. The analysts expect this trend to stop in June. “Some of that might have reflected poll workers, and were that to be the case, it could persist into June given ongoing elections,” they wrote. “However, state-level employment data shows employment rose in almost every state to some degree in May, so this could also reflect the difficulty of seasonally adjusting the normal summer rise in government employment.”

JP Morgan economists are skeptical that the World Cup provided more than a small boost to hiring. In addition, “the most strength came in food services. That industry added essentially no jobs between 2019 and mid-2025 despite a steady rise in real restaurant consumption. The implied productivity gains may have run their course, and what could be happening now is simply that hiring in the industry is returning to long-run trends.”

More broadly, “one factor that calls for some caution is the notion that there could be a summer slowdown, with the three-month average in private jobs having bottomed in August in each of the last two years,” they wrote. “In addition to a small sample size, the pattern of monthly weakness hasn’t broken down across months in the same way each year, nor across the same industries, so we don’t have high confidence here.”

Vanguard’s Hirt expects a greater pullback in hiring than the consensus, with job gains in the neighborhood of 50,000: “While we’ve had a favorable first half of the year, we would expect some softness to start coming up over the next couple of months, and we do expect an under-consensus number for Friday.”

Additionally, Hirt thinks that unusually mild weather earlier this year likely pulled forward hiring in construction and leisure and hospitality, meaning some of the strength already seen will “unwind or normalize” in the next few months. In addition, he expects a data adjustment in the Bureau of Labor Statistics’ birth-death model, which tracks job numbers from business openings and closures, as well as separately tracked new business creation numbers.

Wage Growth to Remain Steady

Economists forecast little material change in the trajectory of the workweek or wage growth. Vanguard’s Hirt expects wage growth to remain at a yearly rate between 3.25% and 3.50%. Some areas that may have benefited from wage growth include artificial intelligence and construction, though he says they are merely contributors, rather than drivers. “We’ve seen some modestly stronger wage growth, some modestly stronger hiring in those sectors, and we definitely think that areas like the construction trades have been benefiting from some of the data center buildout,” he says.

The Federal Reserve

Heading into the jobs report, expectations have shifted toward the Fed raising the federal-funds rate at least once in 2026 from its current target rate of 3.50%-3.75%. Fed officials are seen as having shifted their focus away from concerns about a soft economy toward inflation that remains stubbornly higher than they would like.

“Job creation is effectively meeting the size of the labor force,” Vanguard’s Hirt says. “We would take that as a description that the labor market is well-balanced. I think there’s clearly more focus on the inflation side of the mandate currently.”

At Bank of America, economists see another strong jobs report pushing the Fed to raise rates more aggressively than the market currently expects. “If our forecast is correct, this will be the fourth consecutive monthly increase in jobs, with private payrolls averaging a solid 109,000 this year,” they wrote. “The downside labor risks that prompted last year’s rate cuts have not materialized. Combined with sticky inflation, that strengthens the case for reversing those cuts. A strong jobs report would likely push markets toward our call for three hikes in 2026.”

{kind=link}