- In late June 2026, Deere & Company (NYSE: DE) was added to the Russell 1000 Defensive Index and the Russell 1000 Value-Defensive Index, reflecting its classification within defensive and value-oriented segments of the US equity market.

- This dual index inclusion may broaden Deere’s shareholder base by attracting rules-based and defense-focused investors who track or benchmark against these Russell indices.

- We’ll now examine how Deere’s new status in defensive value indices could influence its existing investment narrative and risk profile.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Deere Investment Narrative Recap

To own Deere, you generally have to believe in long term demand for high tech farm and construction equipment and the company’s ability to defend its margins despite tariffs, pricing pressure, and softer large ag cycles. Its addition to the Russell 1000 Defensive and Value Defensive indices does not materially change the near term story, where the key catalyst remains adoption of higher margin precision agriculture tools, and the biggest risk is prolonged weakness in North American large ag and competitive discounting.

Among recent announcements, Deere’s May 2026 guidance for full year net income of US$4.5 billion to US$5.0 billion is most relevant, because the new defensive index inclusion will be interpreted against that earnings range. If end market conditions or tariff costs push actual results toward the lower end of the range, the “defensive” label may be questioned, whereas delivering within or above that band could reinforce the appeal of Deere’s new role in value defensive benchmarks.

But while the new defensive label sounds reassuring, investors should be aware that Deere’s tariff burden and North American large ag exposure could still…

Read the full narrative on Deere (it’s free!)

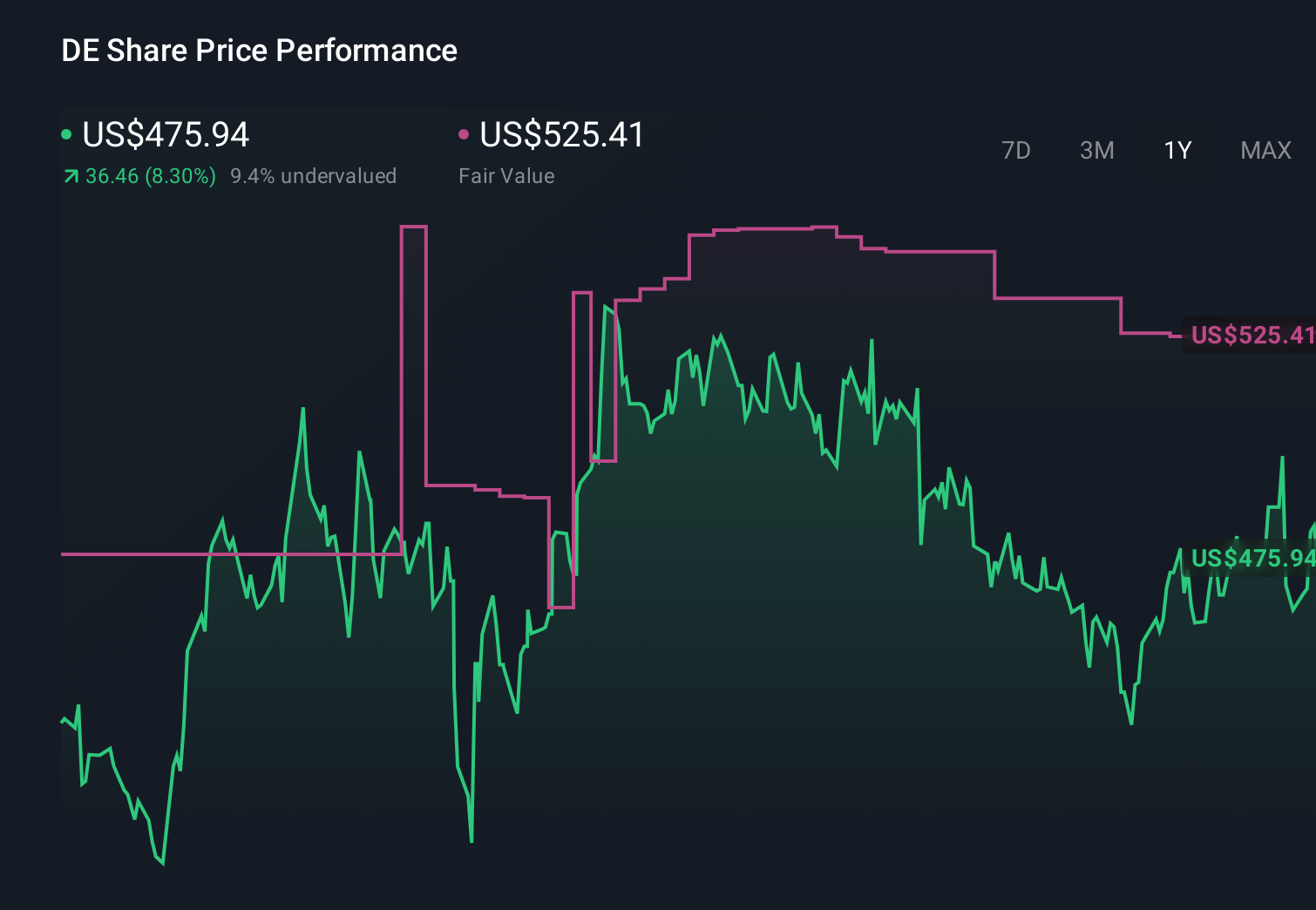

Deere’s narrative projects $48.4 billion revenue and $9.3 billion earnings by 2029. This requires fairly flat yearly revenue and about a $4.5 billion earnings increase from $4.8 billion today.

Uncover how Deere’s forecasts yield a $644.21 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the lowest tier analysts were already cautious, expecting roughly flat revenue near US$45.6 billion and earnings of about US$6.1 billion by 2029, and you can see how that more pessimistic view might look quite different once Deere’s new defensive index status and tariff risks are fully reflected.

Explore 4 other fair value estimates on Deere – why the stock might be worth just $644.21!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Source: Original Article

{kind=link}