As some of you might be watching the England match replay on BBC2 this morning, I won’t spoil the result. But I can’t control the comments! The replay is over now, so congratulations to England and good luck against Norway on Saturday night! Great news for pubs and bookies.

In company news, it’s reported that the easyJet (LON:EZJ) board have agreed in principle to a takeover at 690p per share.

The first three bids from US investment firm Castlelake were at 560p, 600p and 625p. These were all rejected out of hand.

The fourth bid, at 650p, was the one that triggered the easyJet board to start sharing information with Castlelake.

The latest proposal is at a premium of nearly 50% compared to the easyJet share price just prior to the Iran war. So I don’t think that Castlelake can at this stage be accused of opportunistically trying to pick it up “on the cheap” in the aftermath of the war.

Overnight market movements:

-

The FTSE is up unchanged at 10,665

-

S&P 500 is unchanged at 7,500

-

Brent crude (September) is up 0.1% at $72.05/bbl

-

Gold is down 0.6% at $4,150/oz

-

Bitcoin is up 0.7% at $63,150

Mark Simpson joins me today.

Wrapping it up there, cheers! Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

|

Smiths (LON:SMIN) (£7.9bn | SR64) |

Second tranche of the £1bn share buyback programme, with value up to £400m, will commence shortly and is expected to be completed by the end of calendar year 2026. | ||

|

easyJet (LON:EZJ) (£4.23bn | SR44) |

The financial terms of the Fifth Proposal (£6.90 per share in cash) are at a value that the Board would be minded to recommend to easyJet shareholders. Proposal is subject to satisfaction or waiver (by Castlelake) of a number of customary pre-conditions. | TAKEOVER (AMBER/GREEN =) (Graham) Castlelake, as a major player in aviation leasing, are very well qualified to understand what they are buying for £6.90 per share. If they are willing to pay that amount, I’m sure there is a good chance that the true economic value is higher. But I also couldn’t blame fund managers and the Haji-Ioannou family for voting in favour of this deal, if a firm offer materialises. It’s not obviously a bad offer, and it’s materially higher than the LSE has been willing to price the stock for a long time. |

|

|

Greatland Resources (LON:GGP) (£4.11bn | SR93) |

Production of 79,099oz Au and 3,573t Cu for full-year production of 328,986oz Au and 14,594t Cu. Full-year gold production was 6% above the top end of the 260,000 – 310,000koz FY26 guidance range. AISC is still to be finalised. | ||

|

ITV (LON:ITV) (£3.1bn | SR90) |

Sale of the ITV Media and Entertainment business to Sky for a total consideration of up to £1.6bn, made up of: £1.2bn cash, Sky’s Love Production business valued at £200m, and contingent consideration of up to £200m. Enables a cash return to shareholders of around 25p per share. Transaction expected to complete in H2 2027. | TAKEOVER (AMBER/GREEN =) (Graham)

Sky is owned by the US media giant Comcast (NSQ:CMCSA) and so this can be viewed as yet another US takeover of a UK company. This is another case where I can’t make much of an argument against the proposal. There is a logic behind separating out the linear channels from the production studios, sending the channels over to Sky but also swapping in a Sky production studio that makes complementary content. And it’s a nice payday for ITV shareholders. The only negative outcome is it further reduces the value of the listed stocks we get to analyse on the LSE. |

|

|

Raspberry PI Holdings (LON:RPI) (£1.64bn | SR51) |

Tim Powell was most recently CFO of Alpha Group International. | ||

|

Ocado (LON:OCDO) (£1.55bn | SR21) |

Tim Steiner to continue as CEO through the start of FY28 and remain actively involved through 2029. Succession planning process to conclude around the start of FY28 (i.e. around December 2027). | ||

|

Kosmos Energy (LON:KOS) (£920m | SR37) |

In Ghana, the third well of the 2026 campaign was completed and came online in mid-June, two weeks later than initially planned. Initial production rates have been very strong, 20,000 bopd. The next well in the program has been completed and production is expected imminently. Jubilee production to reach c. 90,000 bopd. Net debt at the end of Q2 fell to c. $2.56bn. | ||

|

AEP Plantations (LON:AEP) (£595m | SR99) |

New £8m buyback. The previous buyback programme was completed in June. | ||

|

Avon Technologies (LON:AVON) (£540m | SR44) |

$10.8 million order from an existing European NATO nation under the NSPA framework contract to support the ongoing modernisation of protective capability for military personnel and includes FM50 twin-filter Air Purifying Respirators, FM61EU filters, and accessories. Underpins expectations for FY2027. | AMBER/RED = (Mark) [no section below] This order is through an existing framework agreement and for just 2.9% of FY27 revenue forecasts, so even if it is delivered wholly in that year, it is largely immaterial. Indeed the company confirms that this is already in forecasts as it is said to underpin existing expectations. I took a largely negative view when I reviewed this in May, a very low Value Rank and declining Momentum Rank, made it look like a risky prospect. Since then the share price and StockRank have made a modest recovery. However, with the overall StockRank only 44, and no stand out individual Ranks, it makes sense to remain broadly negative. |

|

|

BTG Consulting (LON:BTG) (£189m | SR86) |

Revenue +10% to £168.5m (8% organic). ADJ. EBITDA +5% to £33.3m. Adj. PBT +6% to £25.0m. EPS +6% to 11.1p. Net Debt £1.0m (FY25: £0.9m net cash). Started the new financial year with encouraging levels of activity in a backdrop of macroeconomic uncertainty which continues to drive demand for restructuring and advisory services, whilst continuing to impact transactional activity. “Expect to deliver a further year of growth in line with our expectations.” |

AMBER/GREEN = (Mark) As a people business, BTG suffers from a lack of operational gearing, as increased revenue often requires additional staff and annual pay rises. This is why PBT growth rates have lagged revenue growth over the last couple of years, and these results are no different. Looking forward, brokers are forecasting mid-single-digit EPS growth, so while the P/E of 10 compares favourably to many listed companies of this size, the PEG of 1.5 suggests this is probably fairly valued at the current price. However, there is a certain attraction to a company that should perform ok whatever the general market conditions. Plus, there appears to be a bit of conservatism in forecasting, and they may well improve their growth rate through acquisition. I’m not convinced that this means we should be paying a higher multiple for this business, but if the EPS grows the share price will likely follow a modest upward trajectory over time. Hence, I’m happy to keep our broadly positive view. |

|

|

Knights group (LON:KGH) (£162m | SR72) |

U/L Revenue +28% to £207.7m (+7% organic). U/L EBITDA +20% to £51.5m, U/L PBT +19% to £33.2m. EPS +17% to 28.1p. Net Debt £65.4m (FY25: £64.8m). “Positive start to the year; look forward to delivering continued organic growth, complemented by value-enhancing acquisitions.” |

AMBER = (Mark) The more I looked into these results, the less I liked them. The net debt, combined with the lack of operational gearing and the lacklustre growth forecasts, suggests it is probably fairly valued for a people business at the current price. If we include possible acquisition-led growth, the question arises of whether we should rely on adjusted figures, where the company asks us to ignore multiple ongoing costs associated with acquiring and reshaping the companies they are buying. Including acquisitions while taking a more conservative approach to adjustments puts us back in a position where the shares look fully valued. That said, it is hard to argue that this is materially over-valued, even if sector peer Gately looks much better value at current prices. Roland was neutral when he reviewed this last in January, so I don’t see any reason to differ from that view. |

|

|

Seascape Energy Asia (LON:SEA) (£62.6m | SR34) |

Executive Chairman, James Menzies, will be taking a medical leave-of-absence for an initial three-month period following a cycling accident. Geraldine Murphy, currently Senior Independent Director, has been appointed Interim Non-Executive Chair with immediate effect. No other board changes. | ||

|

Batm Advanced Communications (LON:BVC) (£49.3m | SR80) |

Three-year contract extension with a leading US broadband operator for $1.3m. |

AMBER = (Mark) [no section below] |

|

|

One Health (LON:OHGR) (£33.5m | SR69) |

Revenue +11% to £31.6m. Adj. EBITDA +28% to £2.6m. Underlying EPS +10% to 14.98p. Cash £11.1m (FY25: £11.4m). “The Company remains well funded to deliver further organic growth and execute the carefully planned roll-out of the first surgical hub to accelerate growth and improve profitability.” | ||

|

Fiinu (LON:BANK) (£20.9m | SR2) |

Notes the circulation of a letter by Granicus which was sent to a number of shareholders and other interested parties in advance of the Company’s forthcoming AGM, to be held on 24 July 2026. The Board does not agree that the Group’s FY2025 statutory loss is evidence of management failure. Considers it largely due to non-cash impairments that may be eventually recovered. | ||

|

Oriole Resources (LON:ORR) (£18.1m | SR31) |

MB01-S Step-out Drilling Programme Final Results & Completion of Senala Joint Venture Agreement |

Final two holes in the drilling program returned 13 gold intersections including 16.40m at 1.65g/t Au from 116.80m depth. |

RED (Mark) [no section below] |

|

Power Metal Resources (LON:POW) (£13.7m | SR42) |

Molopo Farms Project has been extended until 31 March 2028. 1,600m core drilling program commenced. |

Graham’s Section

Up 10% at 616p (£4.7bn) – easyJet announces Offer Update – Graham – TAKEOVER (AMBER/GREEN =)

As I’ve already discussed in the preamble, there’s been big easyJet news this morning.

While the media already had their hands on it, we have RNS confirmation to dissect now.

It’s a joint announcement by eastJet and Castlelake:

The Board of easyJet plc… and Castlelake, L.P… announce that they have reached an agreement in principle on the key financial terms of a recommended cash offer, pursuant to a further proposal that Castlelake submitted to the Board of easyJet on 4 July 2026 to acquire the entire issued and to be issued ordinary share capital of easyJet not already held by Castlelake for £6.90 per share in cash, including a partial unlisted share alternative (the “Fifth Proposal”).

Some key points in the announcement:

1. “Tremendous respect”. Castlelake “has emphasised its tremendous respect for easyJet and its people, along with its intention to support its future growth and transformation to a stronger, more resilient European airline for the benefit of all stakeholders”. I interpret this as a pledge by Castlelake not to engage in asset stripping or unnecessary job cuts, but instead to continue investing in it. Castlelake is “supportive of easyJet’s fleet modernisation programme”.

2. Customary pre-conditions. Castlelake has not made a firm offer yet. Their pre-conditions are standard: due diligence and documentation. Of course, even if these conditions are satisfied, this doesn’t guarantee that there will be a firm offer.

3. PUSU deadline. The PUSU deadline is extended to Monday 3rd August (four weeks from today).

Graham’s view

We aren’t yet at the stage of having “irrevocable undertakings” or letters of intent. So we can’t yet be sure of what major shareholders such as the Haji-Ioannou family think:

All we can say for now is that the Board are happy with the suggested price. Board members such as:

All of the non-Executive directors are currently independent, i.e. there are no representatives of major shareholders such as the Haji-Ioannou family on the Board.

This is important insofar as the Board may not yet know if the company’s shareholders will agree to this price.

I would expect most of the fund managers to support it, as fund managers in general tend to be enthusiastic supporters of takeover offers – and £6.90 is a nearly 50% premium to the pre-Iran war easyJet share price.

The share price this morning is around a 10% discount to £6.90, implying some level of uncertainty as to when and if the takeover might proceed. There will be regulatory hurdles: Castlelake has made a “best endeavours” commitment to obtain any regulatory clearances that are required.

While I personally would not be thrilled to have easyJet leave the LSE, I can’t argue against this takeover proceeding. A premium of nearly 50% against the pre-war price would give eastJet shareholders several years of uncertain returns upfront, in cash.

The counter-argument is that despite the prevailing share prices, £6.90 might still be a bargain for Castlelake.

This proposal values the company at £5.2 billion, when it has a £3.7 billion balance sheet that likely understates the true economic value of airport slots, its existing fleet, and an enormous Airbus order for 157 aircraft along with valuable options to acquire another 100 aircraft.

And from the point of view of earnings, City consensus suggests that earnings per share could soar as high as 61p in FY 2028, which would bring the forward earnings multiple down to 11x.

Castlelake, as a major player in aviation leasing, are very well qualified to understand what they are buying for £6.90 per share. If they are willing to pay that amount, I’m sure there is a good chance that the true economic value is higher.

But I also couldn’t blame fund managers and the Haji-Ioannou family for voting in favour of this deal, if a firm offer materialises. It’s not obviously a bad offer, and it’s materially higher than the LSE has been willing to price the stock for a long time.

ITV (LON:ITV)

Up 1% at 82.8p (£3.1bn) – Sale of ITV M&E Business to Sky – Graham – AMBER/GREEN =

The ITV share price jumped to 77p last November when it confirmed that it was discussing this sale with Sky.

It has been range-bound since then, and today’s confirmation appears to have come as no surprise:

The £1.6bn price tag for the M&E division is as expected, but the details are as follows:

-

£1.2bn cash

-

Sky’s Love Productions business, valued at £200m (this produces shows such as Great British Bake Off and The Piano). The £200m figure is based on an EBITDA multiple of 8x.

-

Contingent consideration of up to £200m, depending on advertising performance in FY27.

The M&E division contains ITV’s terrestrial channels, ITVX, and their YouTube channels.

The result: £950m to be returned to ITV shareholders, or 25p per share.

What’s left? ITV Studios: the production company for Love Island, I’m a Celebrity, etc.

The disposal of M&E “Unlocks value of ITV Studios, which will be a distinctive pure-play global content business, delivering above-market profitable organic revenue growth over the medium term..:”

As part of the deal, there will be a “content supply agreement” with ITV M&E and Sky, including a “minimum spend commitment of £2.1 billion over 2028-2032. So ITV Studios will not have to worry about finding customers for its content for the next few years.

Timetable: expected to complete in H2 2027.

ITV CEO comment:

I am confident that Sky will be a strong and responsible custodian of ITV M&E, building on its heritage while investing in its future and safeguarding the qualities that make ITV so valued by viewers, advertisers and the UK’s creative industries.

Looking ahead, ITV Studios will be well positioned to deliver long-term value to its shareholders through a combination of above-market profitable organic revenue growth and attractive returns to shareholders. This is driven by its world class talent, global scale and a unique IP library, and further supported by a long-term strategic partnership with ITV M&E and Sky, including a £2.1 billion minimum spend commitment.

The small print: there will be £185m of transaction and separation costs over the next 3-4 years, which reduces the net, after-tax cash proceeds to c. £1.05 billion.

ITV’s net debt was £592m as of March 2026, according to the Q1 update.

Without the earnings from M&E, it will have less capacity for this debt, so the first thing it will have to do is pay some of it down: “Proceeds will first be used to de-lever ITV Studios to c.1.5x net debt to EBITDA post completion.”

The valuation multiple for the sale is said to be 5.6-6.4x trailing EV/EBITDA, which is “in line with precedent transactions in the sector”.

Trading update: full year expectations are unchanged.

Graham’s view

Sky is owned by the US media giant Comcast (NSQ:CMCSA) and so this can be viewed as yet another US takeover of a UK company.

However, this is another case where I can’t make much of an argument against the proposal.

There is a logic behind separating out the linear channels from the production studios, sending the channels over to Sky but also swapping in a Sky production studio that makes complementary content. And it’s a nice payday for ITV shareholders.

The only negative outcome is it further reduces the value of the listed stocks we get to analyse on the LSE. This might be partially offset by ITV Studios attracting a higher valuation as a standalone entity.

But it is hard to escape the feeling that the US is becoming a sort of financial black hole, with its major corporations and investors hoovering up almost anything that looks decent in the UK. They aren’t the only cause of the decline in the number and value of UK-listed stocks, but there is no question they have played a role.

The number of UK-listed companies has approximately halved over the past two decades, to the current level of about 1,500. I suppose we should be thankful that there are some buyers for our cheap stocks!

Mark’s Section

Down 3% at 113p (£189m) – Final Results – Mark – AMBER/GREEN =

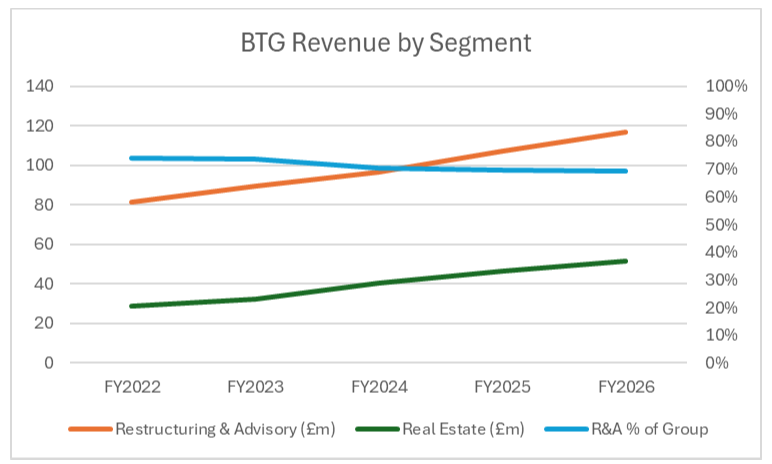

Many investors will recognise this company under its previous name, Begbies Traynor. It changed its name in February 2026 to reflect its expansion from a legacy insolvency firm into a broader, multi-disciplinary financial and real estate advisory practice.

Revenue Trends:

Restructuring and Advisory remains the key revenue driver, accounting for around 69% of revenue. This is down slightly from the 74% a few years ago:

I can’t see how they break out Insolvency from Advisory in historical results, but today they say the restructuring business generated 82% of segmental revenue. Given this, you’d expect these results to be strong in the current weak UK macroeconomic environment. They quote the Insolvency Service statistics to back this up:

National insolvency appointments in the year ended 30 April 2026 were 23,616 (2025: 23,979) with the number of administrations increasing by 12.3% to 1,739 (2025: 1,548), with the increase principally driven by over 190 national appointments associated with the high-profile Market Financial Solutions (MFS) insolvency, a significant number of which are being undertaken by the group. Liquidations decreased by 3.6% to 18,095 (2025: 18,764). (Source: Insolvency Service statistics on a seasonally adjusted basis).

This background is reflected at the revenue level in these results.

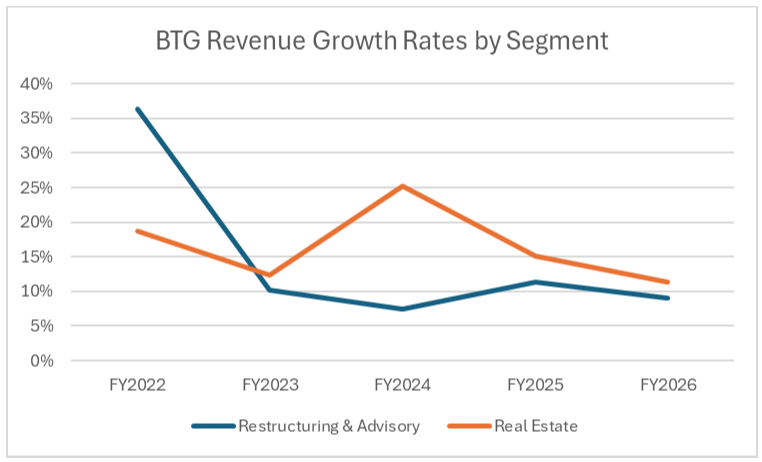

While the Real Estate segment has grown faster overall over the last few years, aided by a focus on acquisitions in this space, the overall pattern of growth is not clear cut:

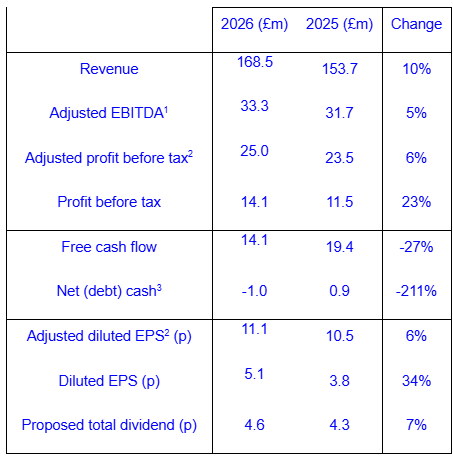

Today’s results:

BTG don’t provide percentage changes in their summary table, but I think it is worth adding these in as they tell a story in themselves:

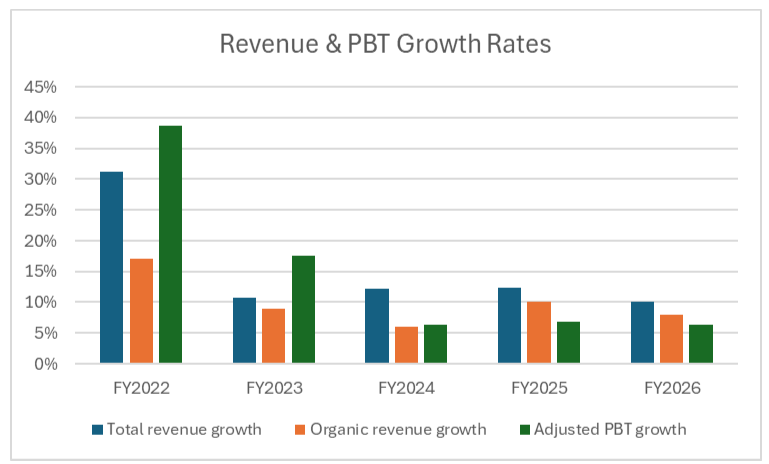

While revenue is up 10%, of which 8% is organic, adjusted profit measures are only up by lower percentages, showing that growth in people businesses almost always comes at the cost of greater staff numbers. In this industry, macroeconomic woes caused by inflation concerns will also lead to higher pay demands and rises in other costs.

Historical Context

This is a pattern that we have seen over the last three years with Adj. PBT growth coming in below revenue growth rates and often below the organic revenue growth rates:

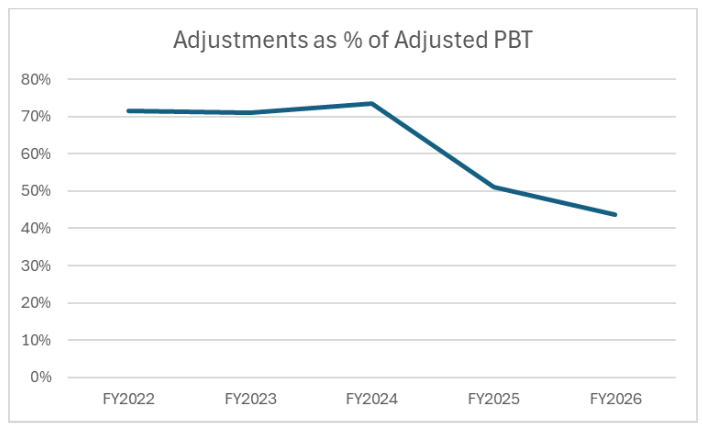

Adjustments

The better news is that the gap between the adjusted and statutory figures is narrowing. Adjustments are still significant, though, and represented 44% of Adjusted PBT last year:

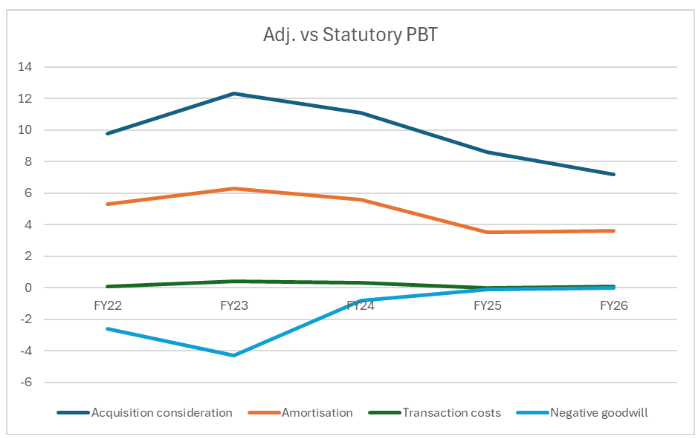

Here are the details:

Overall, these adjustments are a mixed bag, and investors need to make their own minds how they treat these. Personally, I think if I were to use the adjusted figures, I would use the organic growth rates in any valuation to try to balance these impacts.

Outlook:

This is what they say:

We have started the new financial year with continued momentum across the group, supported by current activity levels and pipeline visibility. The backdrop of macroeconomic uncertainty continues to drive demand for our counter-cyclical services, albeit it continues to impact our transactional activity.

This all seems reasonable, but they don’t really say whether they are trading in line with expectations. An explicit statement on this would have been reassuring.

They reiterate their £200m medium-term revenue target but do not specify an actual timeframe or margin expectations.

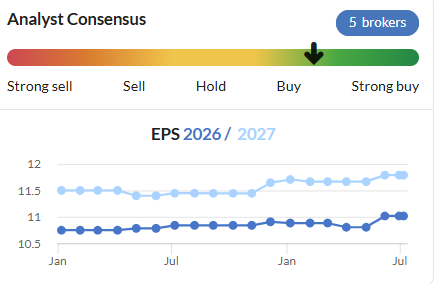

Broker Forecasts

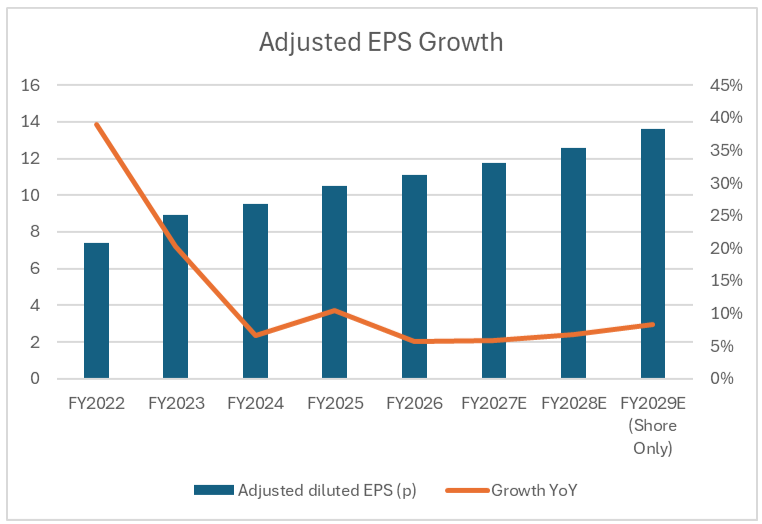

Shore’s note title is “FY26 beats. Outlook positive”, but there is a certain amount of marketing in this assessment, as the actual beat is pretty small, with them saying “revenue & profits have both come in 2% ahead of our expectations”.

Canaccord title their note “Delivering sustainable growth”. However, they don’t see the company reaching the £200m revenue target within their 2-year forecast window. Shore are willing to forecast out an extra year to FY2029 and see them reaching this level then.

However, the EPS forecast growth rate is pretty lacklustre. Canaccord are more pessimistic than Shore, but the net result is something like a 6% CAGR of EPS over the next three years, in line with the kind of figures they have been reporting over the last few years:

There may well be a certain amount of conservatism in these forecasts as the consensus tends is marginally positive:

Plus, these won’t include acquisitions, which may bolster growth. However, my previous comments stand here; I think it’s probably best to value the business on organic growth rates if one is to use the adjusted EPS figures.

Balance Sheet:

The company has dipped into net debt, but this is relatively minor, and they spent £8.1m on acquisitions, paid £6.9m on dividends and bought back £1.2m of shares in the period.

Overall, the balance sheet looks reasonable with a current ratio of 1.3. However, this is a people business where there is little tangible asset backing to protect the downside in extremis.

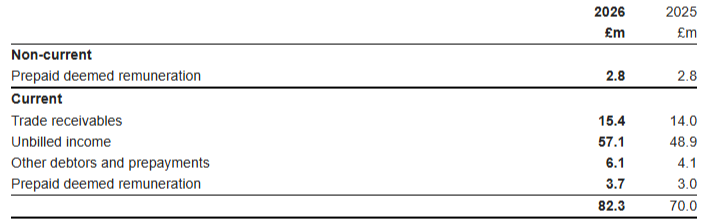

One thing to be wary of is that unbilled income makes up a significant proportion of receivables, and this has risen this year:

This is part of how insolvency practitioners operate; billing is tied to court processes, creditor approvals, or case milestones. However, I would still have liked to see some reassuring commentary given the jump.

Valuation

Canaccord has a 166p Price Target, but I can’t see details of how they get there. This looks punchy to me, given that this would be a 14.3x P/E for a company where their own forecasts expect around 6% medium-term EPS growth.

The current share price of 113p, with a P/E of around 10 and a PEG ratio of 1.5, probably bakes in expectations of either beating current forecasts or making some good-value acquisitions along the way. The very average Value Rank also reflects this:

However, the Quality Rank is high, reflecting the asset-light nature of people businesses, and the generally positive trend.

A modestly growing 4% dividend may also be attractive to some investors.

Mark’s view

I struggle to get excited by this company. They never seem to shoot the lights out apart from the odd exceptional year, such as 2022. Forecasts are for much the same as recent trends: mid-single-digit EPS growth. On a pure valuation basis, a PEG of around 1.5 seems like fair value for such a people business.

However, there is a certain attraction to a company that should perform ok whatever the general market conditions. Plus, there appears to be a bit of conservatism in forecasting, and they may well improve their growth rate through acquisition. I’m not convinced that this means we should be paying a higher multiple for this business, but if the EPS grows the share price will likely follow a modest upward trajectory over time. Hence, I’m happy to keep our broadly positive view. AMBER/GREEN

Up 3% at 194p (£162m) – Full Year Results – Mark – AMBER =

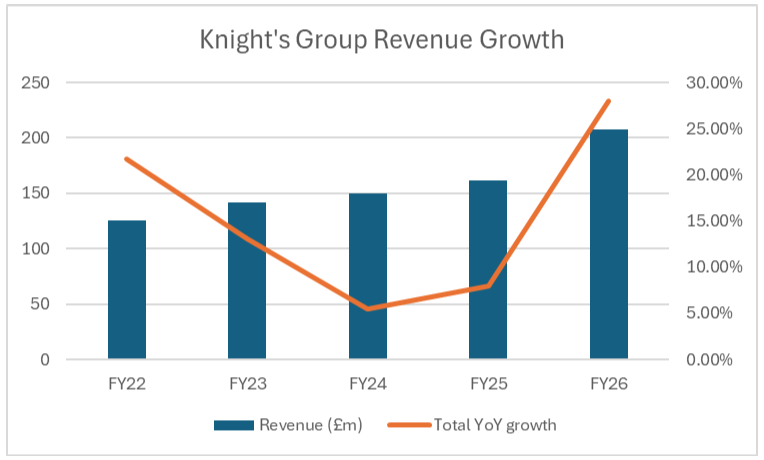

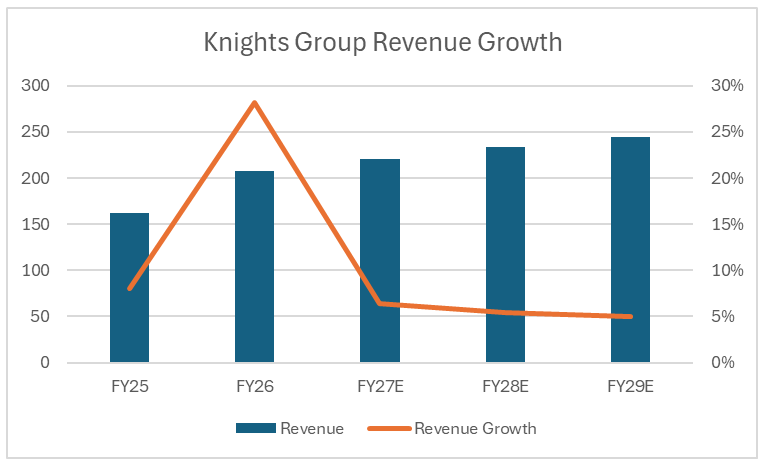

Knights Group is another acquisitive people business. Revenue in these results shows a strong increase of +28%:

However, organic growth is a much more modest 7%, although H2 is said to have delivered 12% growth, showing a certain amount of momentum. These are also significantly higher than in previous years, for which organic growth was negligible.

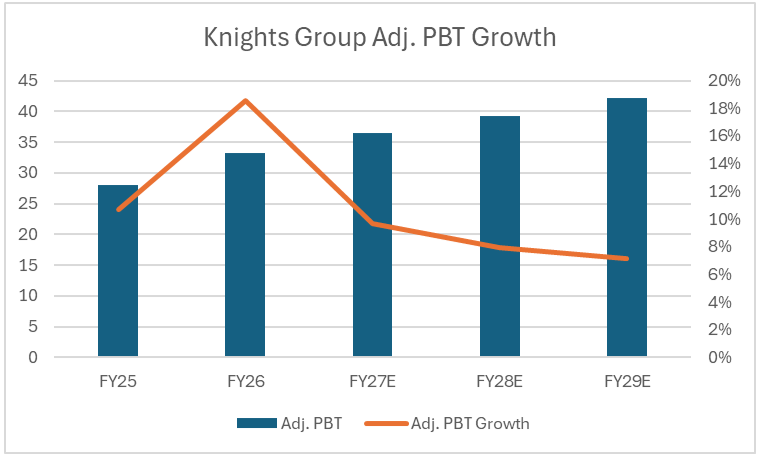

Similarly to BTG, there is a lack of operational gearing with growth rates reducing as you go down the income statement:

· Underlying EBITDA increased by 20% to £51.5m (FY25: £42.9m)

· Underlying PBT up 19% to £33.2m (FY25: £28.0m)

· Underlying basic EPS increased by 17% to 28.14p per share (FY25: 23.95p)

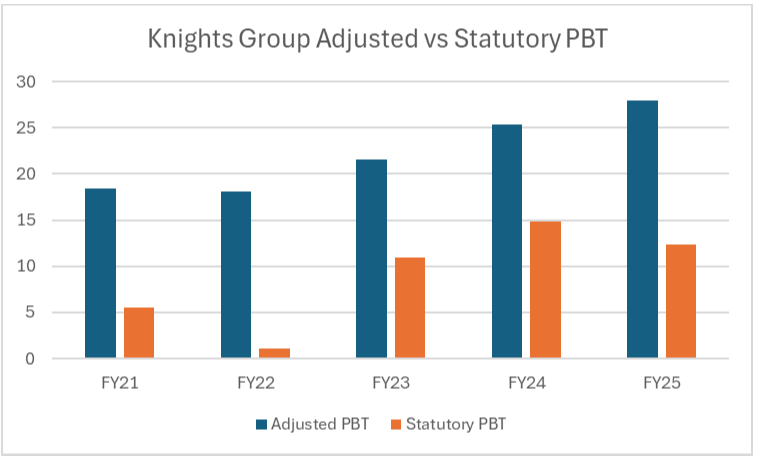

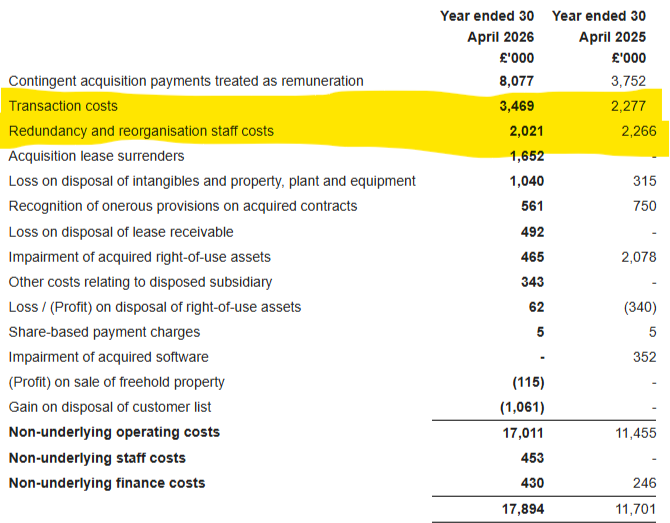

Adjustments:

Again, this is a company where the gap between adjusted and statutory figures is large:

IFRS 3 applied to contingent acquisition payments is again a big one. However, Knights’ transaction costs are significant and there are recurring restructuring costs that the company would prefer us to ignore in these results:

Plus, there is a tail of smaller adjustments, suggesting that everything they buy isn’t always in the condition they would like.

Overall, the adjustments here are less defensible for a business that has grown almost entirely through acquisitions over the last few years than at BTG, and investors should definitely consider using either statutory figures or organic growth rates in any valuation.

Outlook:

This sounds good:

Positive start to the year; look forward to delivering continued organic growth, complemented by value-enhancing acquisitions

But they make no mention of actual figures or if they are in line with expectations.

Broker Forecasts:

The only note I can see is paid-for research from Equity Development which is a well-written note with plenty of detail. However, the forecasts themselves are uninspiring. Lacklustre revenue growth:

And modest operational gearing:

Valuation:

As part of their roll up strategy, Knights have taken on increasing levels of debt:

Excluding lease liabilities, net debt in these results is similar to last year at £65.4m, and they say their Net debt / EBITDA banking covenant ratio is at 1.5x. Their bankers must have confidence in their cash generation as they also report that they have “extended our revolving credit facility to £159m from £100m, committed until July 2029, providing the flexibility to continue to pursue our growth strategy.”

This, plus a current ratio of over two, suggests that there is no immediate concern over their insolvency. However, this debt should be taken into account in any valuation.

As should the £17.1m in cash acquisition payments which will likely be made over the next three years.

Equity Development have a Fair Value estimate of 315p per share for the company, based on a peer group comparison. They calculate an EV/EBITDA of around 5 for Knights, versus around 7 on average for other UK-listed people businesses. However, the chosen peer group looks optimistic. For example, it includes shipping broker Clarkson, which is in a completely different industry and has a significant moat from its scale and data. Knights’ valuation is currently closer to BTG Consulting or FRP Advisory, which are probably more stable and less risky businesses overall.

The closest listed peer to Knights is almost certainly Gately, which is on an EV/EBITDA of 3.4 on the same forward basis, according to Equity Development. It may be that the entire listed legal roll-up industry is mispriced by the market. However, on the surface, the peer group comparison suggests that investors seeking exposure to this industry should consider buying Gately rather than Knights!

Mark’s view

I wanted to be positive about a company delivering 28% revenue growth on a single-digit forward P/E. However, the more I looked into this company, the less I liked it. The net debt, combined with the lack of operational gearing and the lacklustre growth forecasts without acquisitions, suggests it is probably fairly valued for a people business at the current price. If we include possible acquisition-led growth in our valuation, this raises the question of whether we should rely on adjusted figures when the company asks us to ignore multiple ongoing costs associated with acquiring and reshaping the companies they are buying. Including acquisitions while taking a more conservative approach to adjustments puts us back in a position where the shares look fully valued.

That said, it is hard to argue that this is materially over-valued, even if sector peer Gately looks much better value at current prices (assuming forward forecasts there are realistic). Roland was neutral when he reviewed Knights last in January, so I don’t see any reason to differ from that view. AMBER

Source: Original Article

{kind=link}