As stock prices continue to soar, fears of an AI bubble are increasing. The tech bubble of the 1990s was driven by fear of missing out (FOMO). This time, fabulous earnings momentum (FEMO) is driving tech stock prices higher. An earnings-led meltup like this should be more sustainable than a P/E-led meltup fueled by irrational exuberance. That’s especially true of FEMO meltups, like this one, that have been climbing a wall of worry.

Consider the following:

(1) Stock prices. The S&P 500 closed at a record 7,580.06 on Friday, 11.0% above its 200-day moving average (chart). The equal-weight index closed at 8,442.40, 7.2% above its 200-dma. Both are elevated and may pull back.

On May 10, we raised our year-end target for the S&P 500 from 7,700 to 8,250. We are sticking with it.

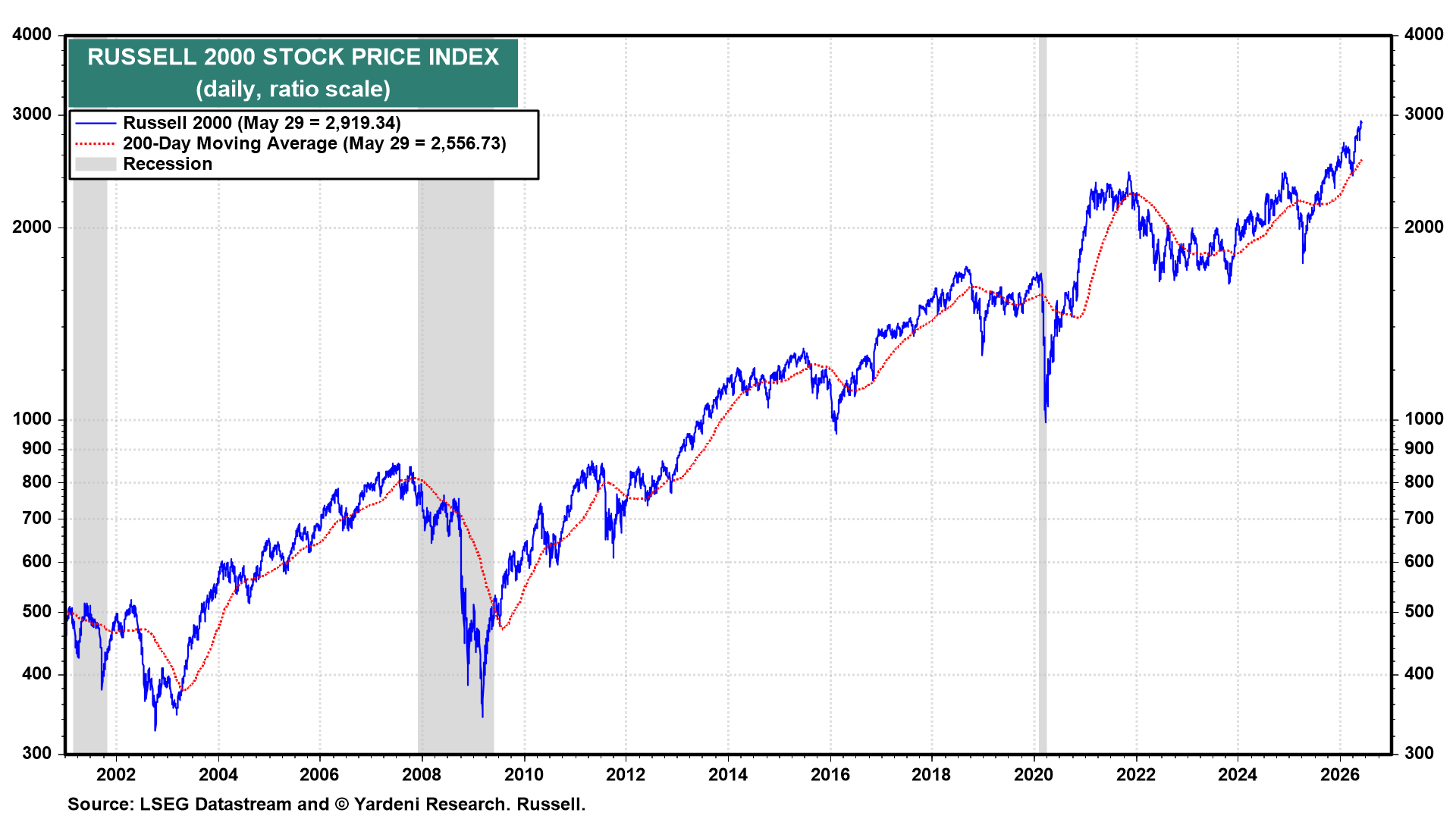

On Friday, the Russell 2000 closed at a record 2,919.34, 14.2% above its 200-dma (chart). We expect that the stock market’s breadth will continue to broaden once the Gulf War ends.

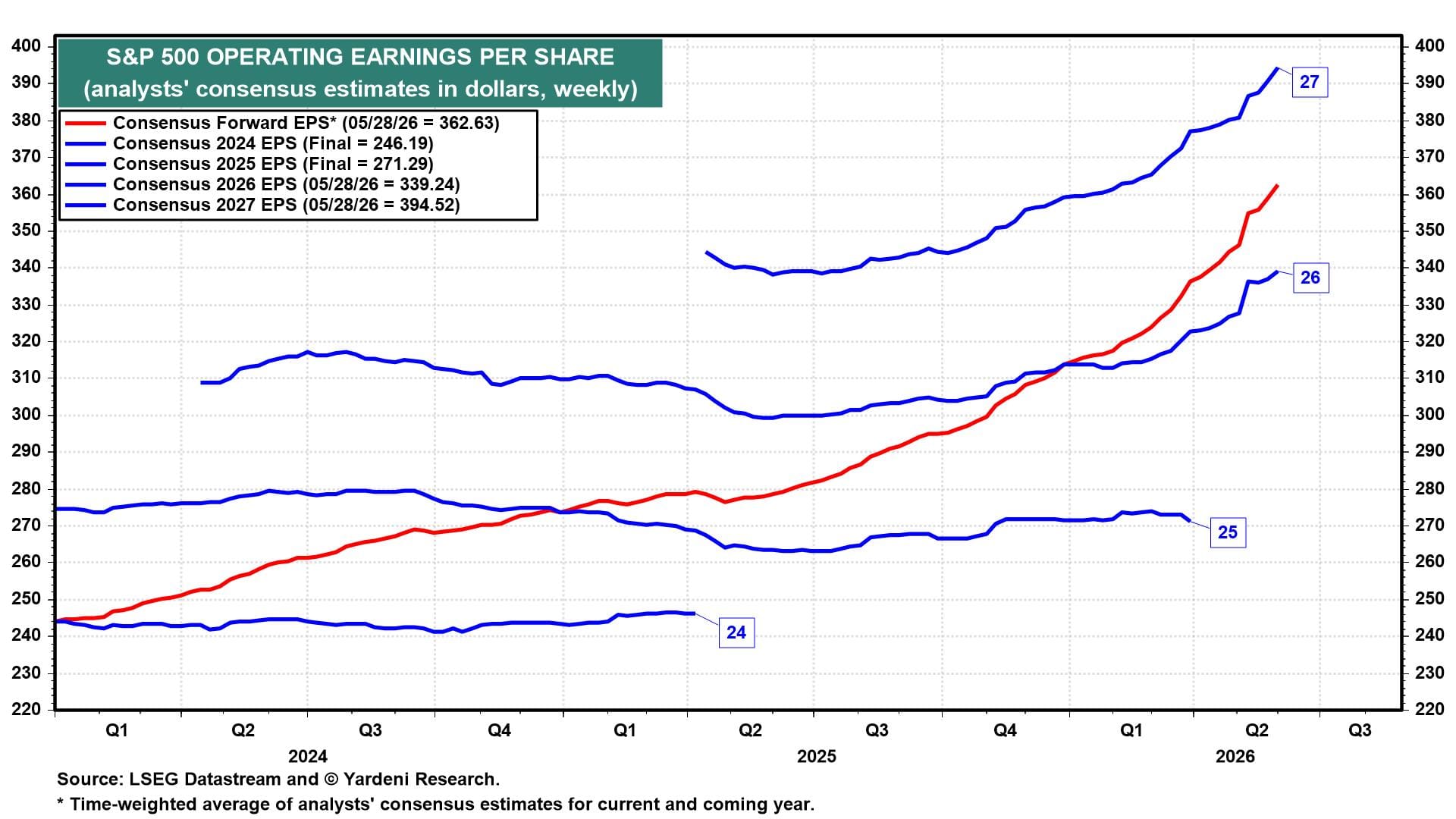

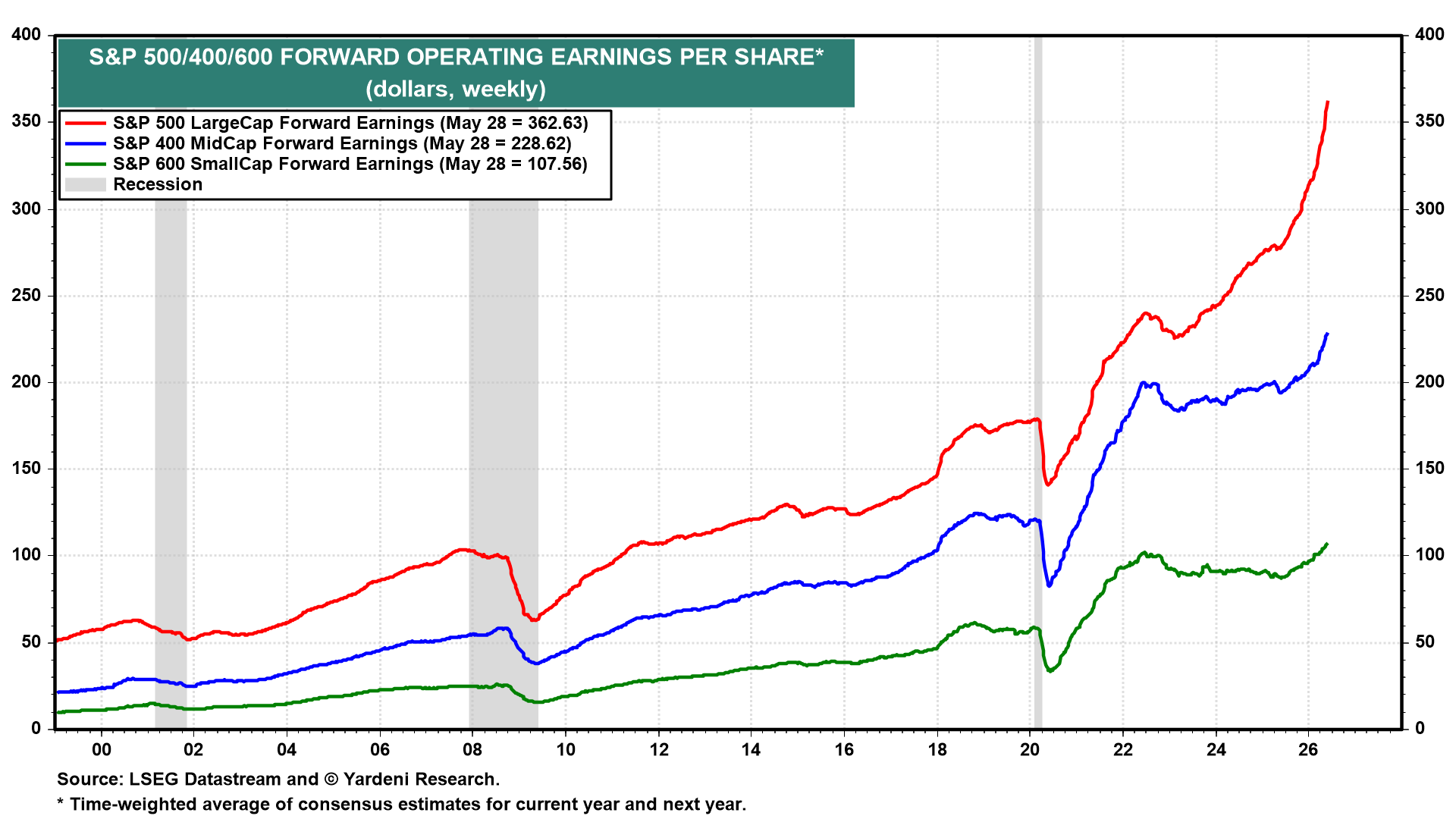

(2) S&P 500/400/600 earnings. S&P 500 forward earnings is at a record high. The latest analysts’ consensus has S&P 500 operating EPS at $339.24 for 2026 and $394.52 for 2027 (chart). When we raised our year-end S&P 500 target to 8,250, we raised our comparable earnings forecasts to $330 and $375. The analysts are even more bullish than we are. We might have to follow their lead again.

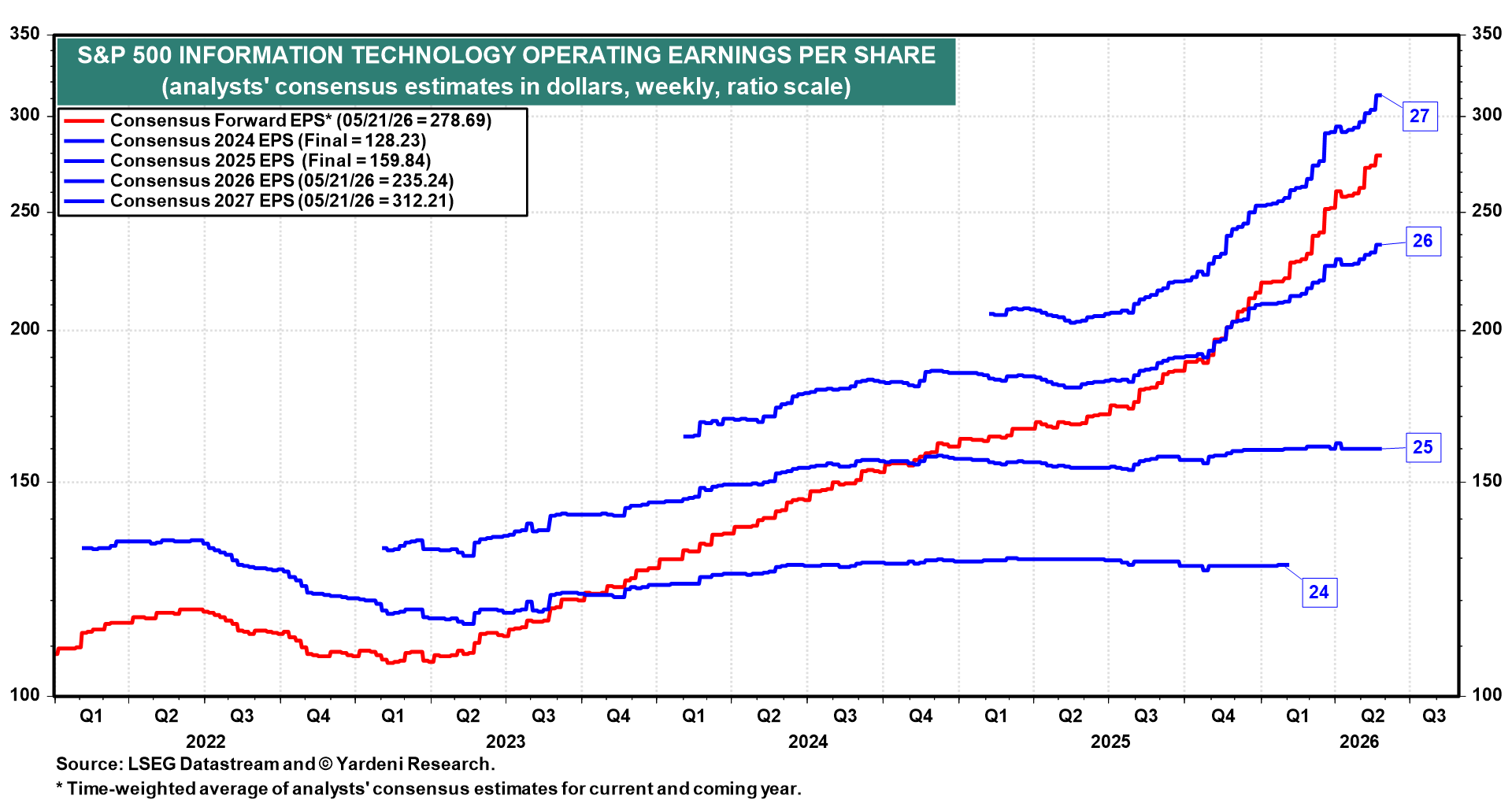

Needless to say, technology is leading the way in the analysts’ FEMO derby. S&P 500 Information Technology operating EPS is forecast to grow 47.2% in 2026 and 32.7% in 2027, after growing 24.7% in 2025 (chart).

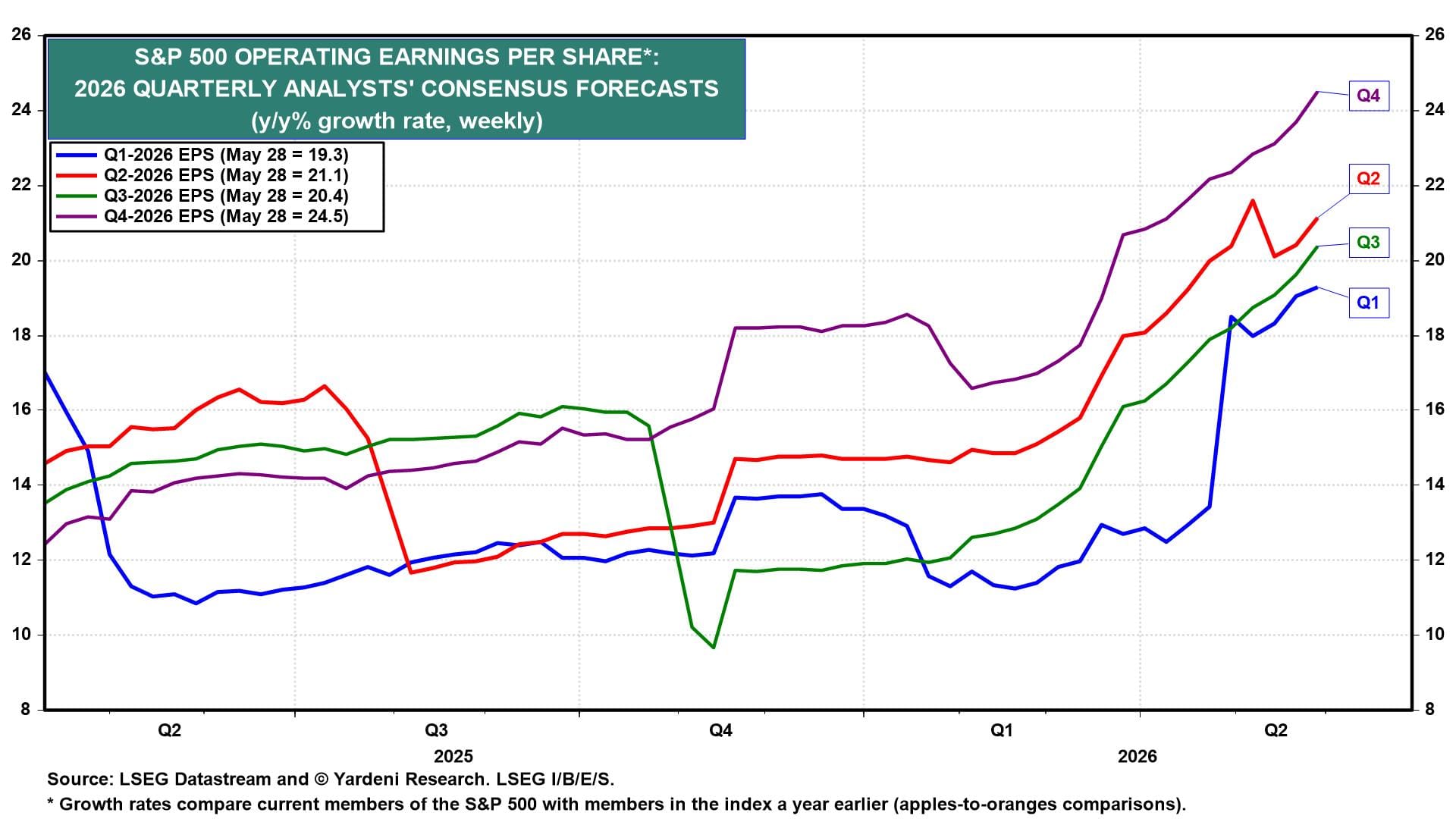

The consensus quarterly EPS growth rates continue to rise. Q1-2026 earnings growth is currently tracking at 19.3% y/y, up from a low of 12.5% in April, just before the start of the Q1-2026 earnings season. Q4-2026 is now tracking at a remarkable 24.5% y/y (chart).

FEMO is running wild across the market-cap spectrum. S&P 400 MidCap and S&P 600 SmallCap forward EPS are also rising rapidly to fresh record highs (chart).

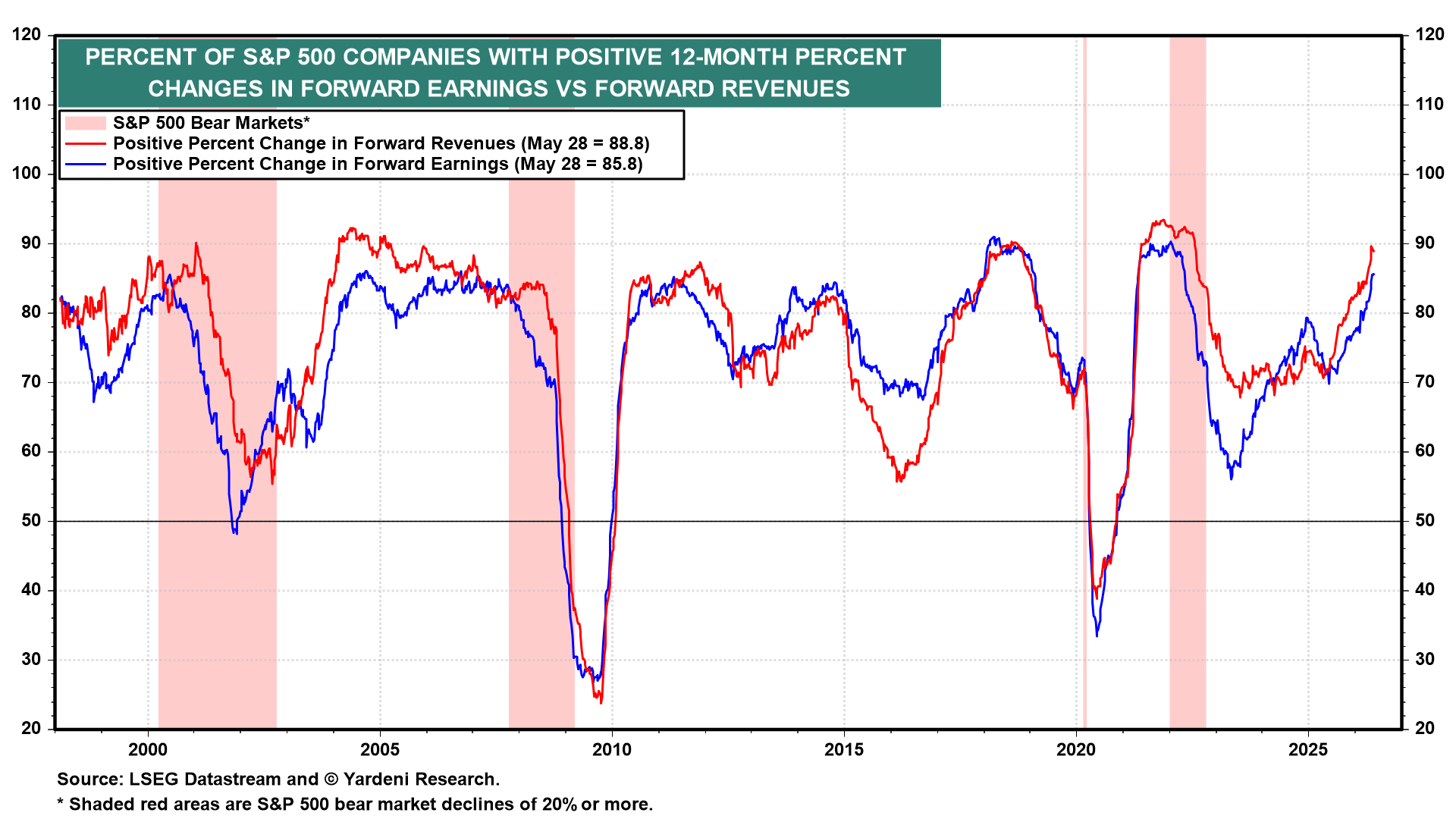

A full 85.8% of S&P 500 companies have positive forward y/y earnings growth, while 88.8% have positive forward y/y revenue growth. Both are near previous cycle highs (chart). The breadth of earnings growth is still improving.

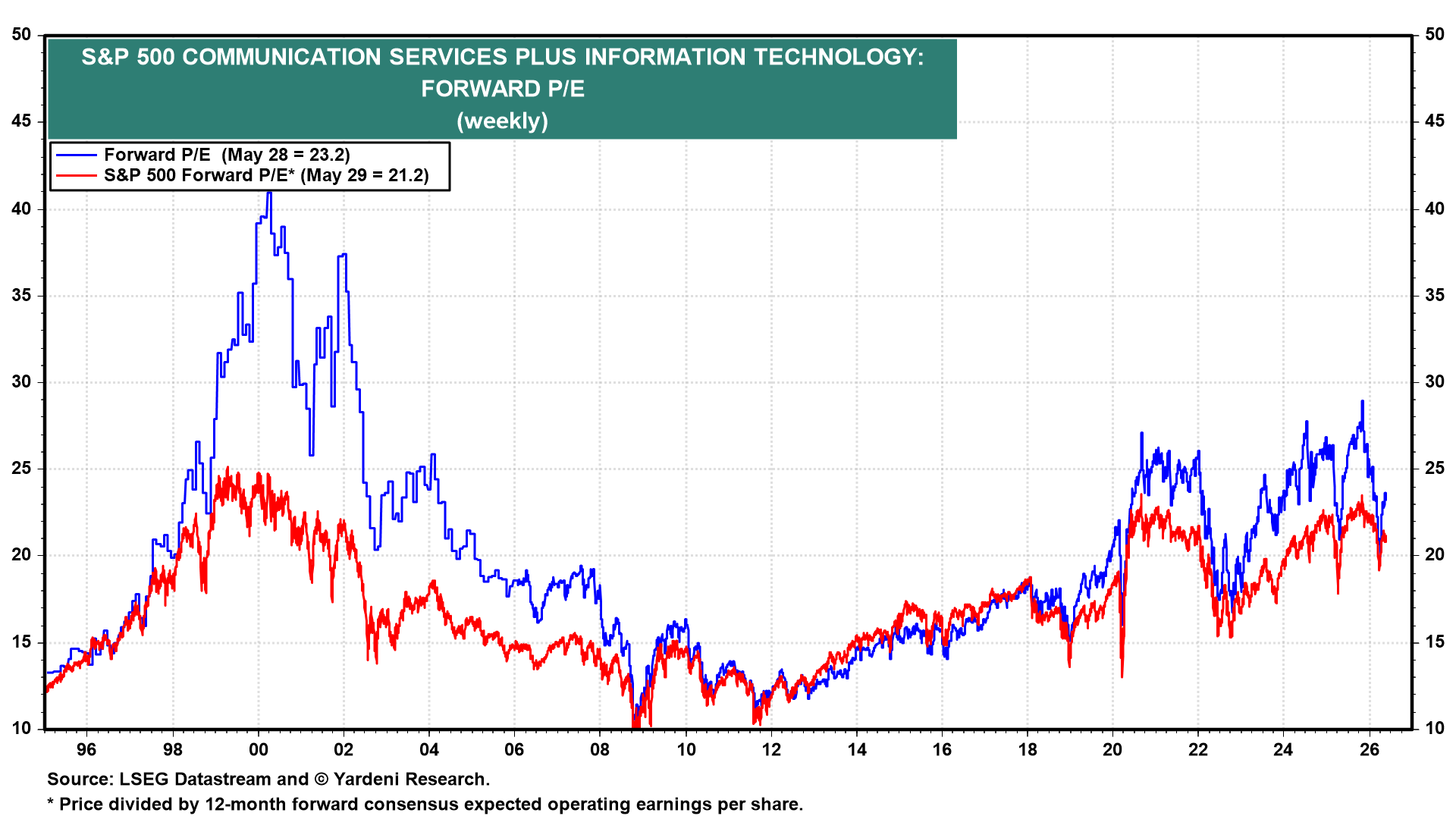

(3) S&P 500 valuation. Despite S&P 500 Information Technology and Communication Services leading the FEMO charge, their combined forward P/E is just 23.2, not much above the overall S&P 500’s 21.2 (chart). In 1998-2000, this same combined forward P/E rose over 40.0. That was FOMO then versus FEMO now. Investors apparently are dumbfounded by the pace of earnings growth and haven’t raised the valuation multiples that they are willing to pay for that growth commensurately. If they do, then we will worry about a bubble.

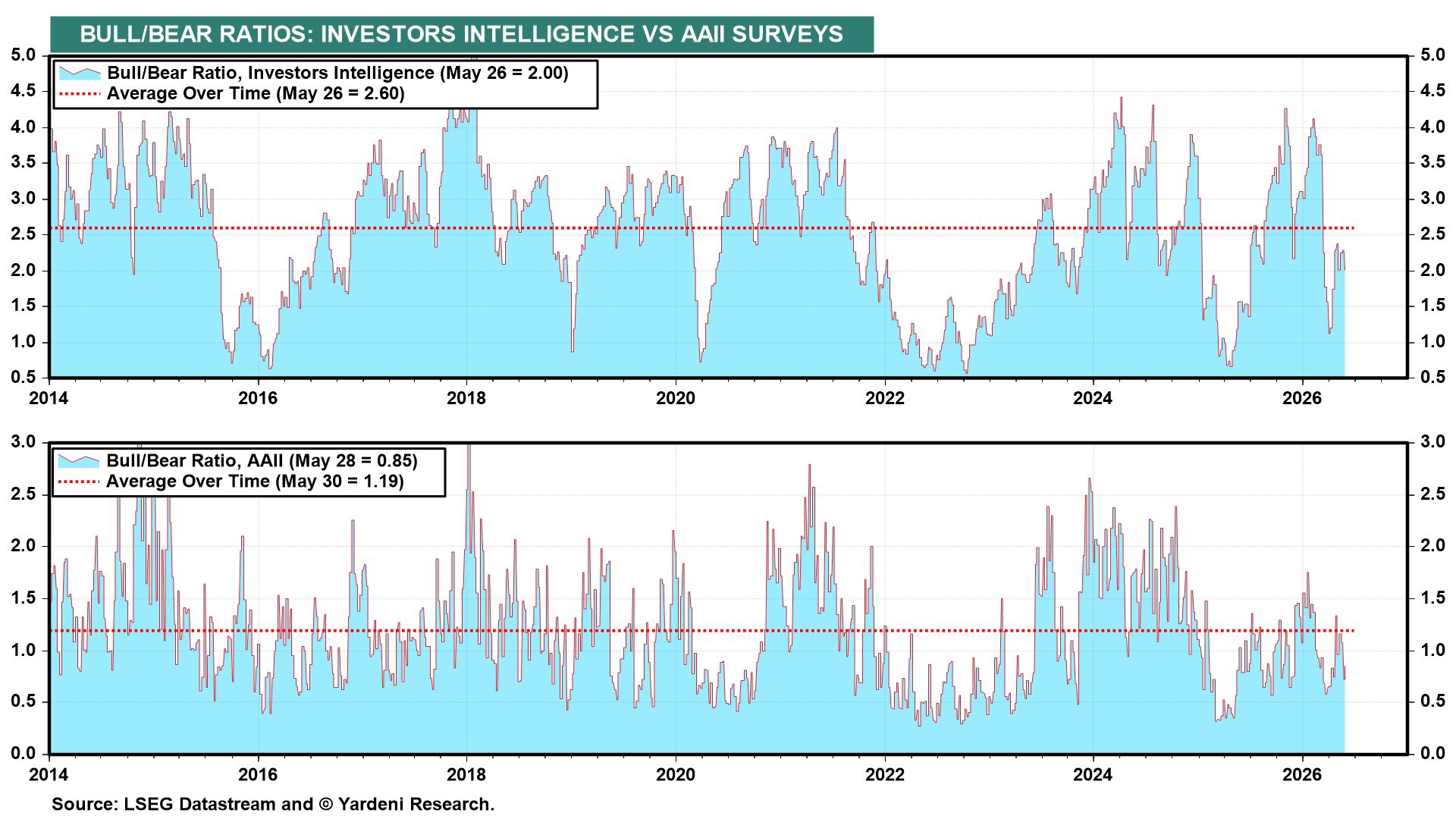

(4) S&P 500 technicals. Investor sentiment is not exuberant. The Investors Intelligence Bull/Bear Ratio is 2.00, which is below its 2.60 long-term average, while the AAII Bull/Bear Ratio is 0.85, also below its 1.19 long-term average (chart). This suggests that there is more upside for stock prices.

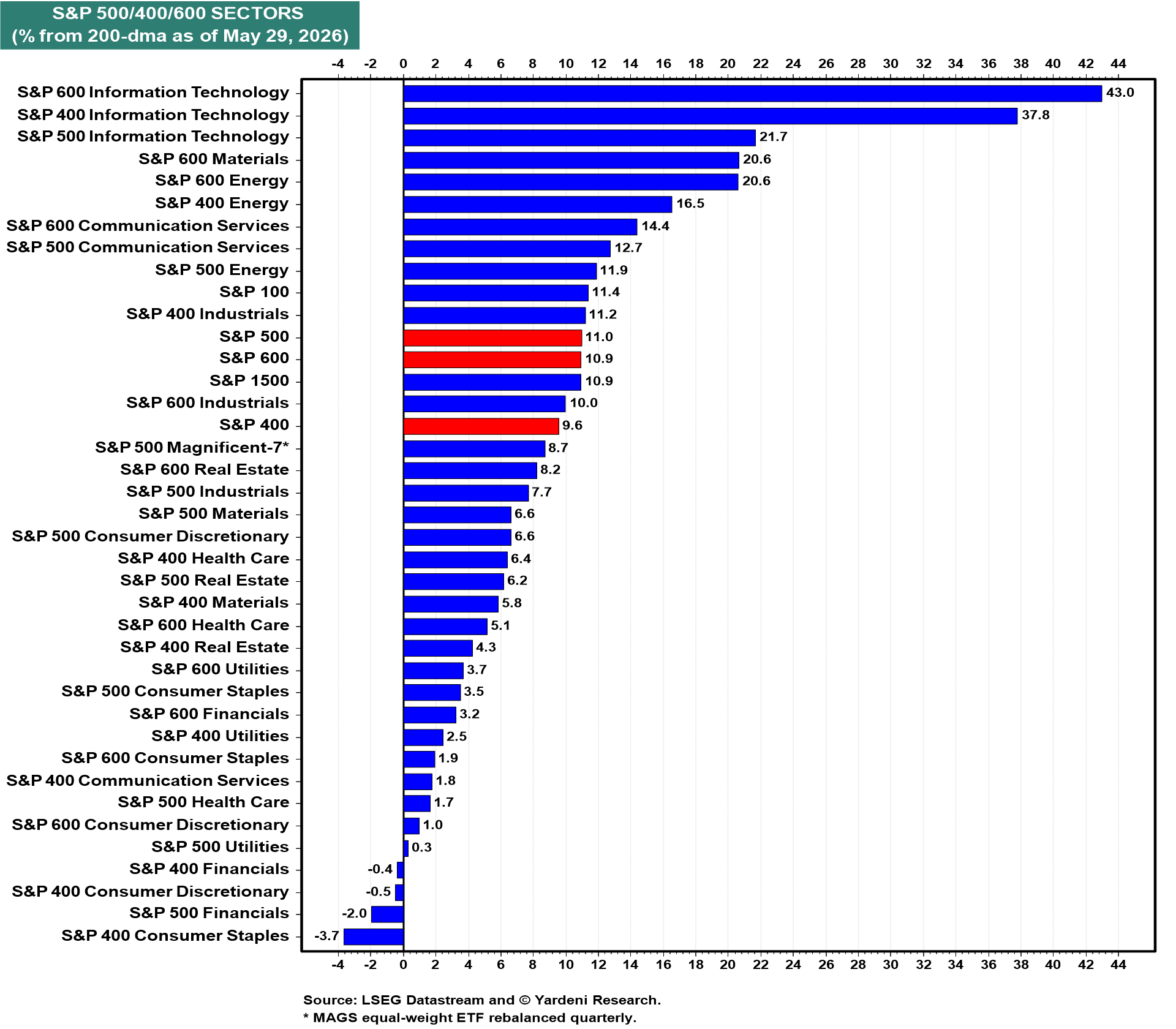

On the other hand, several S&P 1500 sectors look seriously extended compared to their 200-dma (chart).

(5) Bonds. We continue to expect the 10-year Treasury bond yield to mostly range between 4.25% and 4.75% this year (chart). The release last week of April’s hawkish FOMC minutes calmed the Bond Vigilantes, who want the Fed to be more vigilant about inflation.

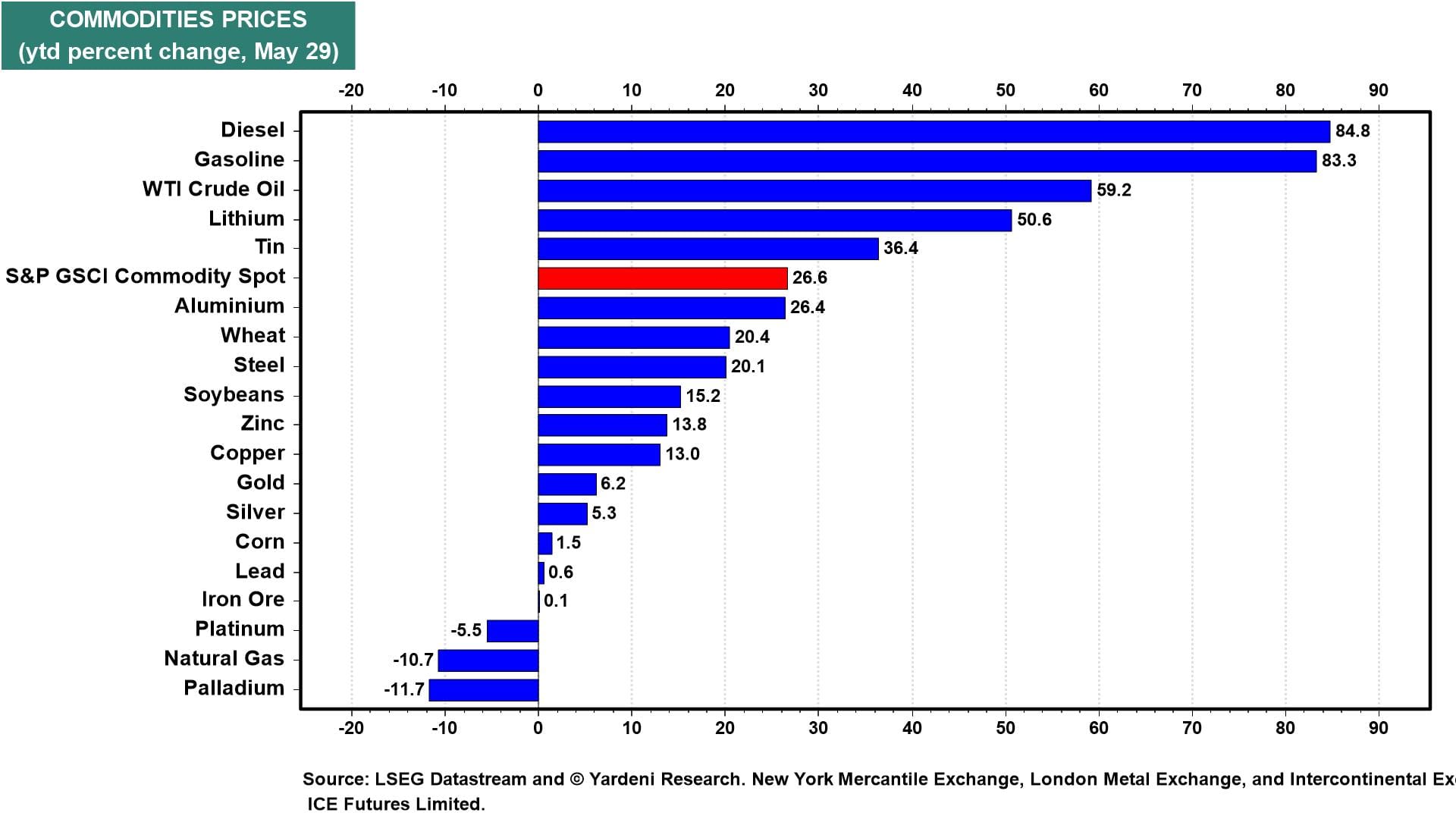

(6) Commodities. The combination of the AI infrastructure boom and the war in the Middle East has boosted commodity prices so far this year (chart).

The price of copper rose to another record high last week (chart). It is at the top end of its bullish channel.

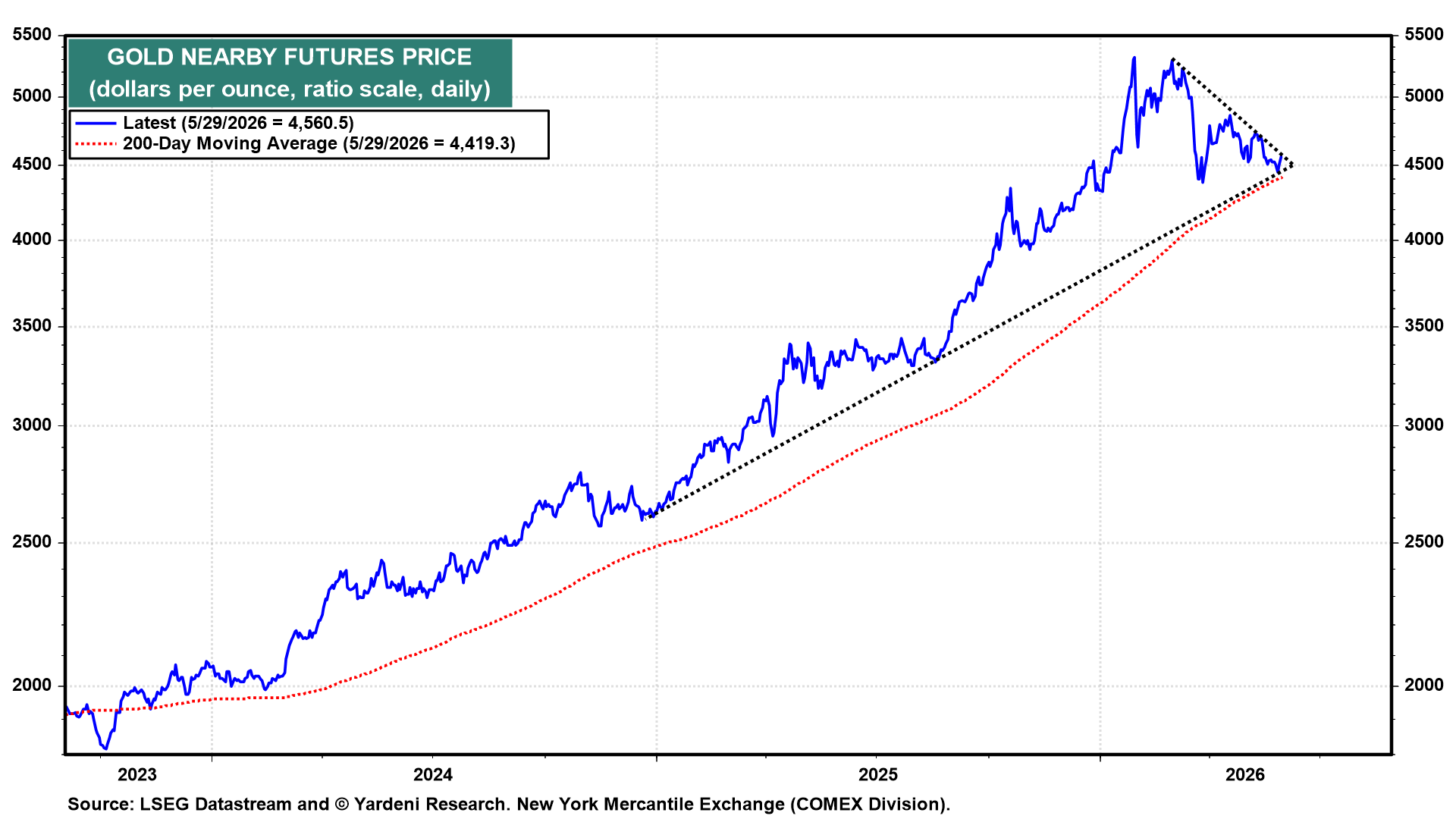

(7) Gold. The price of gold seems to be finding significant support at its intermediate uptrend line, its 200-dma, and its low earlier this year (chart). If Trump agrees to the current ceasefire proposal, which might open the Strait of Hormuz, gold’s price is likely to rise. The war has been bearish, not bullish, for gold.

💡

Join the discussion with Ed below! To leave comments or questions, log in to the Yardeni QuickTakes website and post them at the end of the QuickTakes article. Paid members’ contributions may be featured in our segment, “Ed Answers Your Questions”.

{kind=link}