News of US strikes:

Other:

- Recapping Japan flash PMI – points to modest improvement, but business caution lingers

- Democratic Republic of Congo extended ban on cobalt exports by three months – prices jump

- Fitch Ratings say Australian mortgage arrears showed sharper than usual rise

- Japan’s PM Ishiba will be holding a 9pm Tokyo time press conference

- Tesla launches limited robotaxi trial in Texas on Sunday

- People’s Bank of China sets yuan reference rate at 7.1710 (vs. estimate at 7.1914)

- Japan Jibun bank PMI manufacturing June 2025 preliminary 50.4 (prior 49.4)

- PBOC is expected to set the USD/CNY reference rate at 7.1914 – Reuters estimate

- Bank of Korea will take market stabilising measures if volatility heightens excessively

- Australia preliminary June 2025 manufacturing PMI 51.0 (prior 51.0)

- Fed’s Daly spoke over the weekend – no bombshell comments (I’ll see myself out)

- Trade ideas thread – Monday, 23 June, insightful charts, technical analysis, ideas

- Trump wants a Japan, South Korea, Australia leaders meeting at the NATO summit

- Monday open levels, indicative FX prices, 16 June 2025 – USD up after Trump bombs Iran

- Gold Technical Analysis

- Can You Rely on Weekend Markets? Understanding Weekend CFDs

- Week Ahead Preview: inflation data from the US, Canada, Aus, and Global PMIs

Weekend news was dominated by reports of US military strikes:

-

125 US military aircraft, including seven B-2 stealth bombers as the main strike group

-

Three nuclear facilities targeted: Fordow, Natanz, and Isfahan

-

75 precision-guided weapons deployed, including 14 GBU-57 Massive Ordnance Penetrators (MOPs; ~13,000kg / 30,000lb), dropped on two target areas

-

More than two dozen Tomahawk cruise missiles launched from a US submarine at Isfahan site targets

In the very early hours of the Asia session, FX markets reacted with a mild safe-haven bid into USD. The dollar firmed across the board, with EUR, GBP, AUD, and NZD all gapping lower. JPY and CHF also weakened, while CAD dipped, but found partial support from a rise in oil prices.

At the Globex open (6pm US Eastern), oil prices gapped higher, with Brent briefly hitting five-month highs. US equity index futures opened lower but were quickly bought back, almost fully closing their gaps.

EUR, AUD, NZD, and GBP also recovered early losses, but as the session wore on, these currencies turned lower again—AUD and NZD underperforming most notably.

As of writing, Brent crude has retraced about two-thirds of its gap higher. Technically, Brent broke above a triple top and has since pulled back to retest that level. While oil bulls may be disappointed by the lack of follow-through on such a major escalation, bears should be cautious—they’re still fighting a well-established uptrend. There was a Bloomberg report of two supertankers, each capable of carrying about 2 million barrels of crude, making abrupt U-turns in the Strait of Hormuz on Sunday.

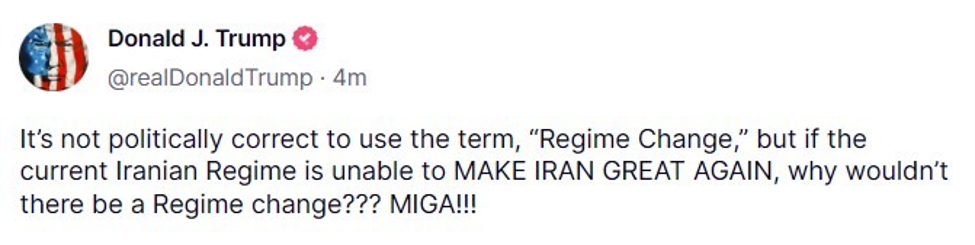

On the political front, President Trump raised the prospect of regime change in Iran, reportedly blindsiding his senior officials. Given the source, the idea can’t be entirely dismissed. If this does become a goal, the Middle East risks entering a sharply more escalatory phase. It’s still unlikely in my view, but with Trump, unpredictability—and follow-through—should never be underestimated.

Other developments:

-

Australia’s flash PMIs showed business activity expanding at a faster pace in June, driven by stronger new orders. However, export orders declined sharply. Sentiment improved, and employment continued to rise.

-

Similarly in Japan, the flash composite PMI rose to 51.4 from 50.2, supported by robust services and an upturn in manufacturing output.

As of writing, USD/JPY is trading near a five-week high. Gold spiked higher at the opening but has since fallen back to be lower on the day.

Brent update:

ForexLive.com

is evolving into

investingLive.com, a new destination for intelligent market updates and smarter

decision-making for investors and traders alike.

{kind=link}